Inside Big Tech's 13Fs: Nvidia's $13 Billion Quarter, Pfizer's BioNTech Exit

Nvidia just took a 4% stake in Intel (INTC). Pfizer fully exited BioNTech (BNTX). Amazon's entire 13F is essentially $3 billion of Rivian (RIVN). The Q4 2025 disclosures from operating companies — corporations that file 13Fs alongside hedge funds because their strategic stakes cross the $100 million threshold — read more like a partnerships ledger than a portfolio.

The headline activity in these filings maps almost cleanly onto press releases: a private placement here, a block trade there, a pre-IPO holding crystallizing into public shares. What changes is rarely a thesis. It's almost always a deal.

The set of operating-company filers covered here — Nvidia (NVDA), Alphabet (GOOGL), Amazon (AMZN), Walmart (WMT), Johnson & Johnson (JNJ), Cisco (CSCO), Merck (MRK), and Pfizer (PFE) — excludes banks, broker-dealers, asset managers, Berkshire Hathaway, and corporate foundations, all of which file in the ordinary course of managing client capital.

Nvidia's portfolio became the chip industry's connective tissue

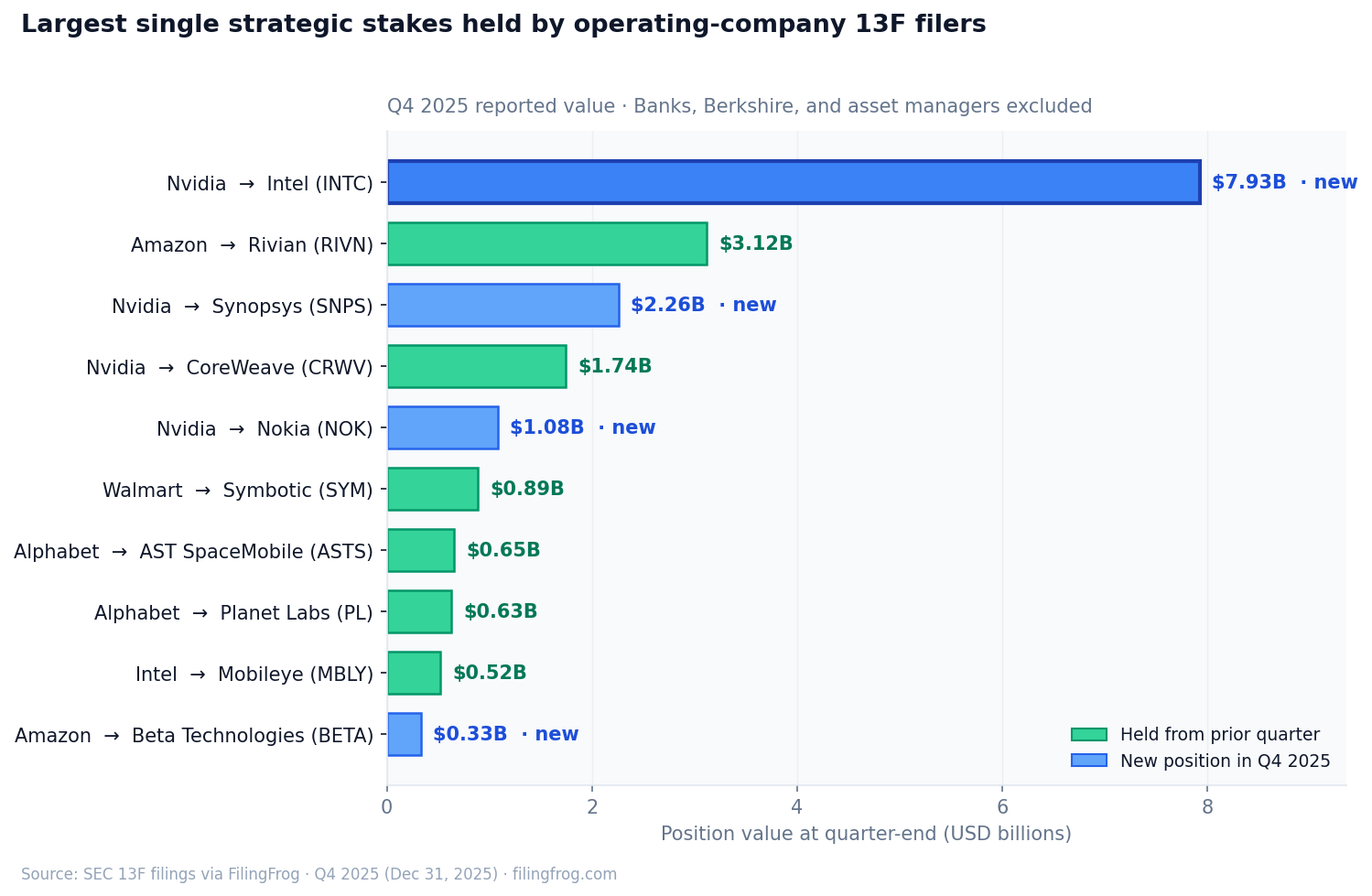

Going into Q3 2025, Nvidia's 13F was small — its largest position was CoreWeave (CRWV) alongside small stakes in Applied Digital (APLD), Arm Holdings (ARM), Recursion Pharmaceuticals (RXRX), and Chinese autonomous-driving name WeRide (WRD). By Q4 2025, three new positions appeared together that account for roughly $11 billion of disclosed value:

- Intel (INTC) — $7.93B, new (214.8M shares)

- Synopsys (SNPS) — $2.26B, new

- Nokia (NOK) — $1.08B, new (166.4M shares)

- CoreWeave (CRWV) — $1.74B, held (24.3M shares unchanged; value moved with the share price)

- Nebius Group (NBIS) — $100M, held

Each of the new positions traces back to a strategic deal. The Intel position is the $5 billion private placement at $23.28 per share that Nvidia announced in September 2025 and the FTC cleared in December — Nvidia took roughly 4% of Intel as part of an agreement to co-develop x86 CPUs and integrate RTX GPU chiplets into Intel system-on-chips. The Nokia position is the $1 billion equity investment Nvidia made in October 2025 at $6.01 per share, paired with a 5G/6G AI-RAN partnership. Synopsys is the chip-design tools company; Nvidia and Synopsys had previously announced a generative AI design collaboration.

What makes the change notable is less the size of any single position than the shape of the portfolio that emerged. The smaller, scattered names from Q3 — Applied Digital, Arm, Recursion, WeRide — were all exited. In their place is a tightly clustered set of stakes in the legacy semiconductor and telecom infrastructure companies Nvidia is most directly partnered with.

Single-name anchors do most of the work

For several of the operating-company filers, one name accounts for almost the entire 13F:

- Amazon (AMZN) → Rivian (RIVN) — $3.12B (88% of Amazon's reported holdings); 158.4M shares unchanged across the quarter

- Walmart (WMT) → Symbotic (SYM) — $892M (92% of Walmart's reported holdings); 15M shares unchanged

- Intel (INTC) as filer → Mobileye (MBLY) — $522M (72% of Intel's reported holdings); 50M shares unchanged

In each case the share count moved a rounding error or not at all — the value differences between Q3 and Q4 came from the underlying stock price, not from any buying or selling. These are post-spinoff or commercial-partnership holdings that the parent has continued to sit on. Amazon's Rivian stake dates to its 2019 commercial-vehicle order. Walmart's Symbotic position came with its 2022 robotics warehousing deal. Intel's Mobileye is the residual stake from the 2022 IPO Intel still controls.

Two smaller names worth noting on the same theme: Walmart added Klarna (KLAR) shares from its September 2025 IPO ($69M, 2.4M shares unchanged), and Amazon picked up Beta Technologies (BETA) at the eVTOL company's late-2025 listing ($332M, new). Both look like positions that arrived through partnership or pre-IPO commitment, then surfaced in 13F disclosure when the underlying shares became publicly traded.

Pharma giants run quiet biotech VC arms

The three large pharmaceutical filers — Johnson & Johnson, Merck, and Pfizer — each disclosed a long tail of small biotech positions. Most are micro-cap clinical-stage names that look more like a venture portfolio than a hedge fund book:

- Johnson & Johnson (JNJ) — 17 holdings, led by Protagonist Therapeutics (PTGX) at $214M and Nanobiotix (NBTX) at $130M

- Merck (MRK) — 12 holdings, led by Personalis (PSNL) at $112M and a still-active Moderna (MRNA) position at $68M

- Pfizer (PFE) — 18 holdings, mostly small clinical-stage oncology and rare-disease names; the largest are ORIC Pharmaceuticals (ORIC) at $44M and Arvinas (ARVN) at $41M

Across the three filers, almost every position carried an unchanged share count between Q3 and Q4 — these are sit-still portfolios. The activity comes when something exits: J&J dropped its Arrowhead Pharmaceuticals (ARWR) position; Merck cleared out LAVA Therapeutics (LVTX). Most of these are stakes taken alongside development partnerships or option agreements, and they tend to fall off the 13F when the partnership concludes one way or another.

Pfizer wound down its highest-profile stake

The exception to the pharma sit-still pattern is Pfizer's largest disposition of the quarter — fully exiting BioNTech:

- BioNTech (BNTX) — $164M position fully sold (1.66M ADRs)

- Tourmaline Bio (TRML) — $61M position fully sold

The BioNTech sale was disclosed in November 2025 as a roughly $508 million block trade representing 54.7% of Pfizer's stake — the position that surfaced from the COVID-era vaccine partnership. The companies remain commercial partners on the mRNA vaccine, but the equity stake has been substantially trimmed.

It's a clean illustration of how operating-company 13Fs work. Pfizer's other quarter-over-quarter positions were largely unchanged in share count. The headline activity sits with one decision tied to one strategic relationship — a partnership entering a new phase, disclosed through a stock disposal rather than a press release.

Alphabet's portfolio splits in three directions

Alphabet has by far the most diverse 13F of the operating-company group — 29 reported positions across three loose buckets:

- Space economy: AST SpaceMobile (ASTS) at $650M and Planet Labs (PL) at $630M, both held unchanged in shares

- Developer tools and AI: Arm (ARM) at $214M, Freshworks (FRSH), UiPath (PATH), GitLab (GTLB), Tempus AI (TEM), Figma (FIG)

- A long biotech tail: Revolution Medicines (RVMD), Maze Therapeutics (MAZE), Prime Medicine (PRME), BridgeBio Oncology (BBOT), Relay Therapeutics (RLAY), Vera Therapeutics (VERA), Sana Biotechnology (SANA), Beam Therapeutics (BEAM), GeneDx (WGS) and a dozen more sub-$15M names

One Q4 exit stands out as worth flagging clearly. Alphabet's $198M Metsera (MTSR) position was dropped to zero — but that exit was M&A-driven, not a sentiment call. Pfizer won a contested bidding war for Metsera in November 2025 against Novo Nordisk, paying roughly $10 billion in cash plus contingent value rights. Alphabet's shares were cashed out in the deal close. When a holder count drops because a deal closed, the meaning is different from voluntary selling.

Explore Ownership ChangesNotes

Holdings are drawn from 13F filings for the quarter ended December 31, 2025, with quarter-over-quarter comparisons against September 30, 2025. The set of operating-company filers covered here excludes banks, broker-dealers, asset managers, Berkshire Hathaway, and corporate foundations — those are financial institutions that file 13Fs in the ordinary course of managing client capital. Position values reflect the value reported on the filing and may differ from the cost basis at original investment. Manager pages, with full per-quarter holdings histories, are available through the Nvidia, Alphabet, Amazon, Walmart, Intel, Johnson & Johnson, Merck, and Pfizer profiles. Cross-quarter ownership shifts at the security level can be browsed at /trends.