A Tech Shakeup in the Making: How Institutions Rearranged the Sector in Q1 2026

For most of the past two years, "tech" moved as a single trade. When the AI narrative was on, the whole basket lifted; when it cooled, it sold off together. The most recent 13F filings show that has changed. Inside the sector, institutional managers are pulling in opposite directions on software and semiconductors — and the gap between them is unusually wide.

Whether the underlying thesis — that agentic AI is starting to eat per-seat software economics — turns out to be right is not yet a settled question. What the positioning data shows is that institutions are no longer waiting to find out.

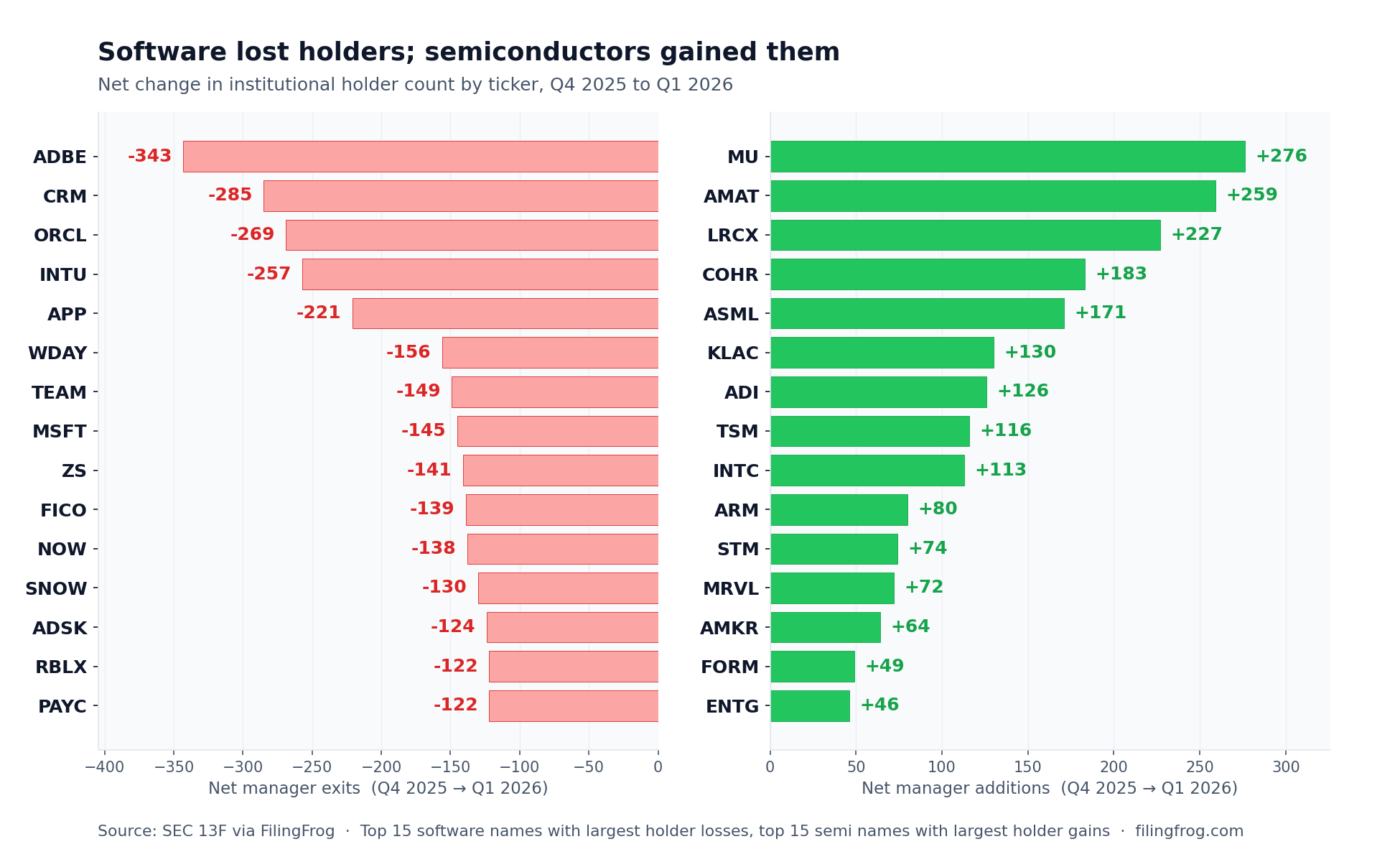

Software lost holders almost across the board

Across a basket of 56 large software names, institutional holder counts fell by 4,712 between Q4 2025 and Q1 2026 — a 7.5% drop in the holder base in a single quarter. The aggregate value of these positions fell by more than a trillion dollars. By contrast, a basket of 40 semiconductor names saw a net gain of 2,034 holders.

The selling extended well past speculative names. Even Microsoft (MSFT) — the largest weighting in most institutional portfolios — saw 145 fewer holders and a $555 billion reduction in reported value. Adobe (ADBE) lost 343 holders, the most of any name. Salesforce (CRM) lost 285. Oracle (ORCL) lost 269.

The pattern is consistent: of 56 software tickers tracked, 52 saw holder counts fall. The few exceptions are explored further below.

Semiconductors absorbed what software let go

In the same quarter, semiconductors saw broad-based additions. The largest gains were not in the names that dominate AI headlines — Nvidia (NVDA) actually lost 53 holders, and Broadcom (AVGO) lost 73. Instead, the additions concentrated in the equipment, memory, and second-tier design names.

- Micron Technology (MU) — +276 holders (+11%)

- Applied Materials (AMAT) — +259 (+10%)

- Lam Research (LRCX) — +227 (+10%)

- Coherent (COHR) — +183 (+21%)

- ASML Holding (ASML) — +171 (+9%)

- KLA (KLAC) — +130 (+7%)

The names doing best are the ones that sell into hyperscaler capital spending. Industry-wide wafer fab equipment spending was revised upward during the quarter, and the largest cloud buyers continued to guide higher infrastructure budgets. That story has not been hard to find, but it appears that institutional positioning only fully caught up in Q1.

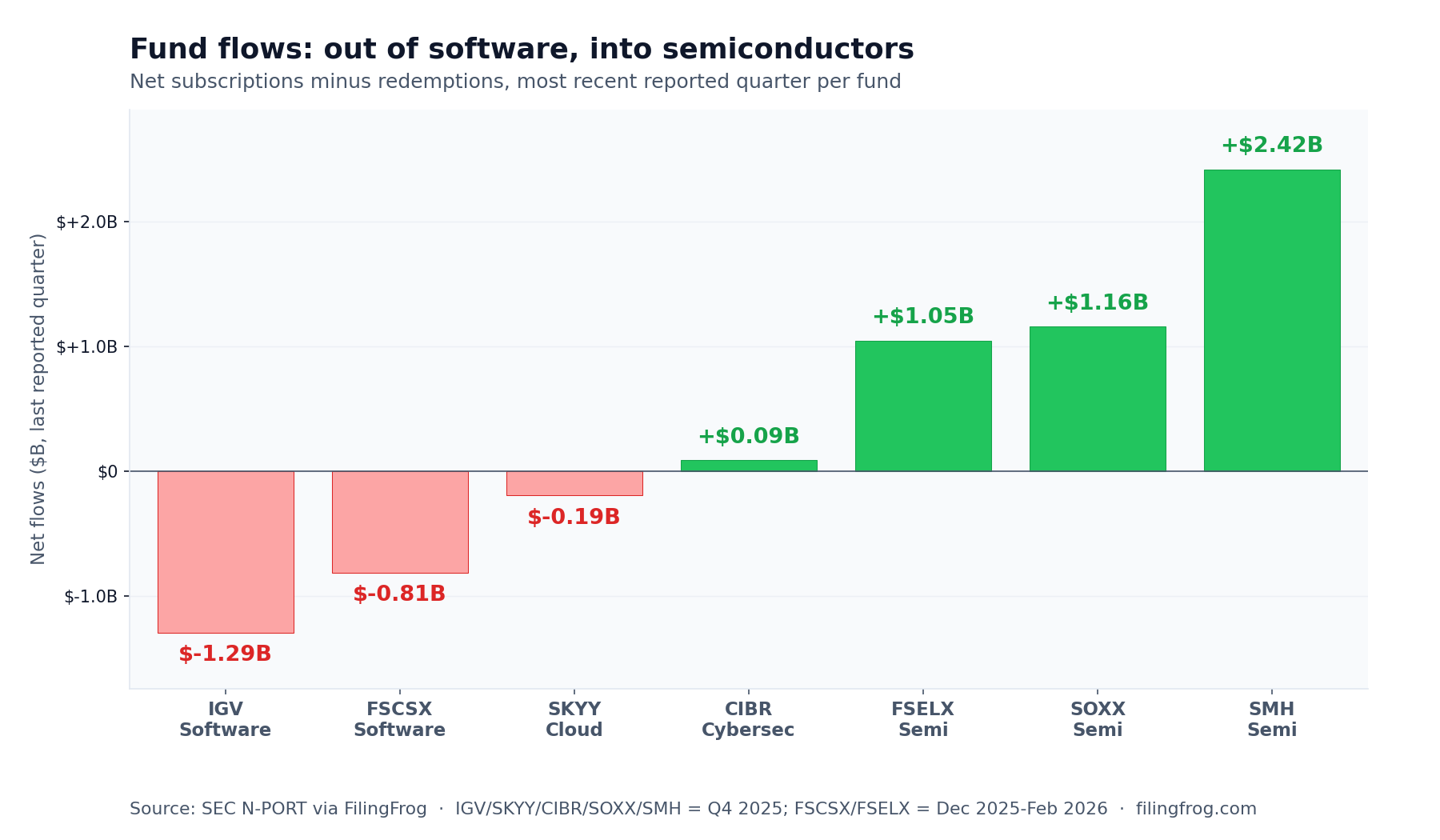

Fund flows moved in the same direction, on the same scale

Fund-level data tells a parallel story. The two largest sector-specific tech ETFs split sharply: VanEck Semiconductor ETF (SMH) took in $2.4 billion in net subscriptions in Q4 2025, while iShares Expanded Tech-Software Sector ETF (IGV) saw $1.3 billion in net redemptions. The actively-managed Fidelity counterparts mirror it almost exactly — Select Semiconductors Portfolio (FSELX) pulled in over $1 billion through February while Select Software and IT Services Portfolio (FSCSX) bled $810 million.

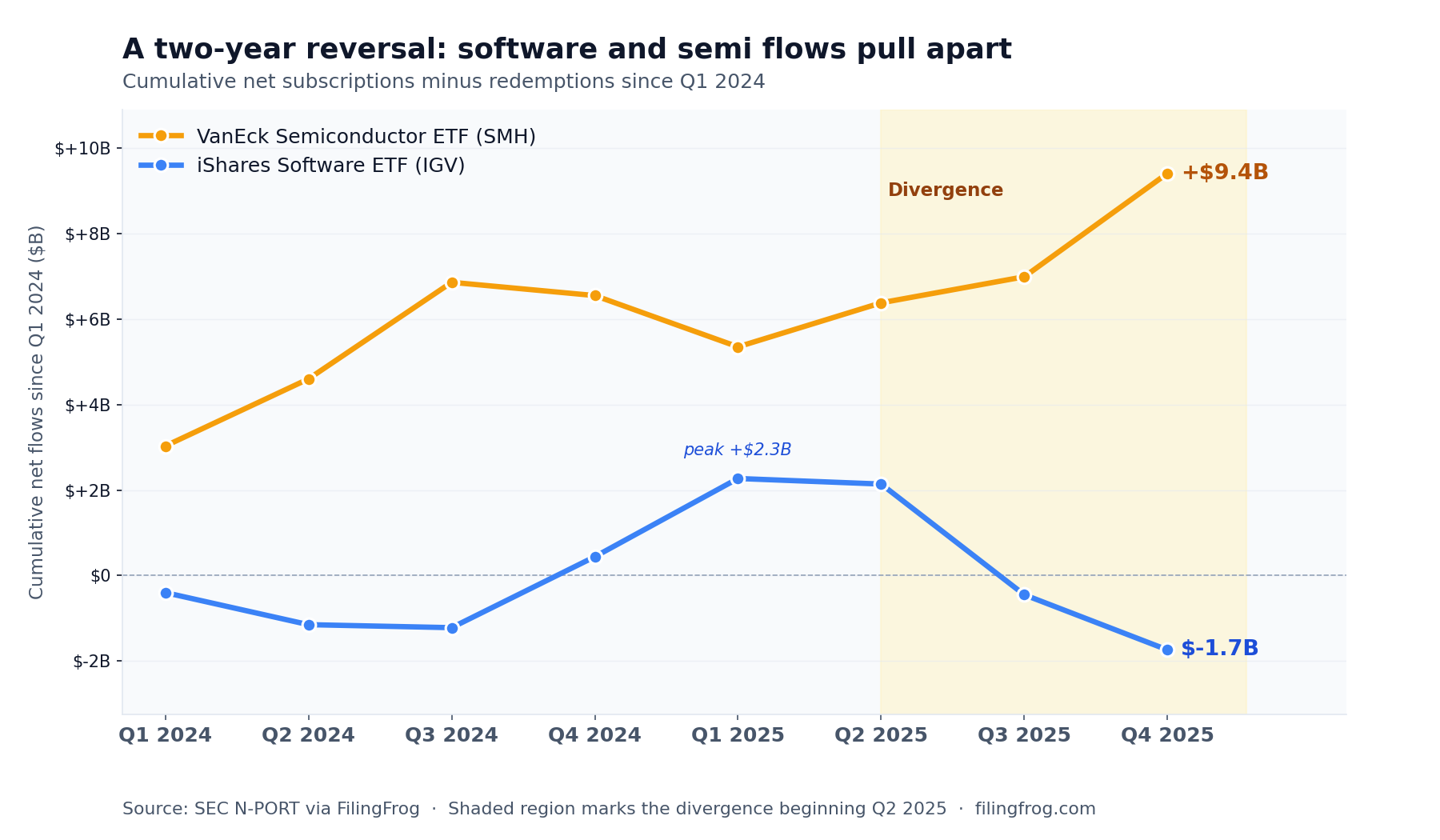

What makes the flow data more interesting than a single quarter would suggest is that it represents a clean reversal. Looked at cumulatively, SMH has pulled in roughly \$9 billion of net subscriptions since the start of 2024 and is still climbing. IGV gathered capital through Q1 2025, peaked at +\$2.3 billion cumulative, then gave it all back — ending the period a net \$1.7 billion below where it started. The two lines were rising together; from Q2 2025 onward, they pull apart.

Why software, and why now

The most cited explanation is the launch of Anthropic's Claude Cowork in early February 2026 — an agentic toolkit positioned to do work that horizontal SaaS platforms have historically billed for on a per-seat basis. The day of the announcement, several services-adjacent names took double-digit single-day losses, and the broader "SaaSpocalypse" framing took hold. Mizuho downgraded Adobe in late April with reference to "intensifying competition" from generative AI. Workday hit a five-year low despite $400 million in AI-related ARR and a record backlog.

The thesis being acted on: if a small number of agents can do the work of a large team, per-seat software economics compress. That is not yet visible in the reported numbers — Salesforce raised guidance, Workday grew its AI book, and Atlassian printed its first $1 billion cloud quarter — but the positioning suggests institutions are not waiting to see how it resolves.

Mega-caps were not spared

The mega-cap platform names — Alphabet (GOOGL), Meta Platforms (META), Amazon (AMZN), and Microsoft — all saw 2% to 2.5% holder reductions. That is smaller than the pure-software basket but consistent with the same direction. It may suggest institutions are taking AI capex risk seriously even for the companies on the receiving end of those budgets.

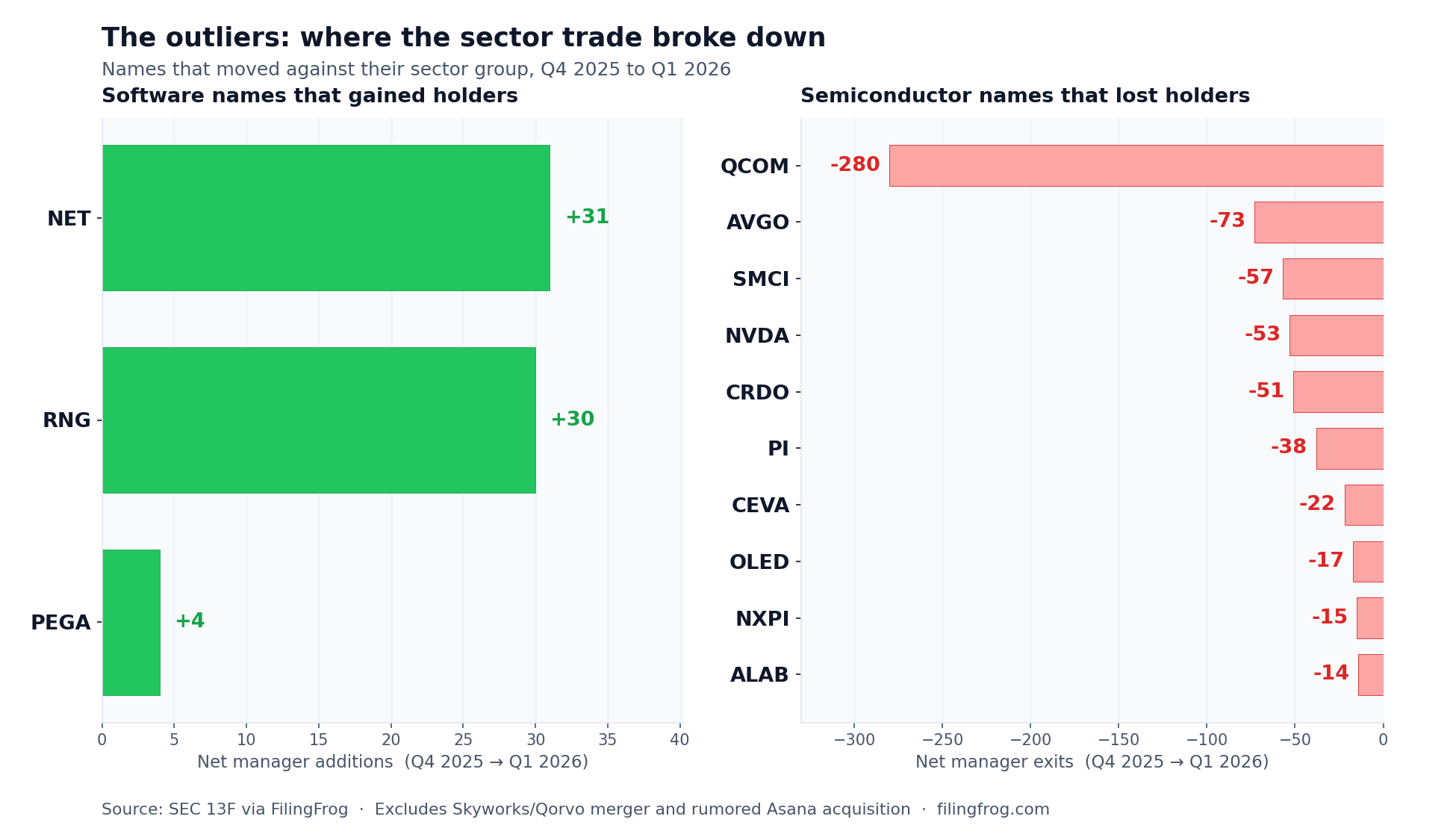

The names that moved against their sector

In any broad sector trade, the most informative names are the ones that don't follow it. Out of the 56 software tickers, four still managed to gain institutional holders. Out of the 40 semiconductor names, twelve lost them — and after excluding the Skyworks/Qorvo merger (mechanical exits as a deal proceeds) and the rumored Microsoft acquisition of Asana, the picture sharpens.

The software gainers share a profile. Cloudflare (NET) and RingCentral (RNG) both picked up roughly 30 net holders; Pegasystems (PEGA) a handful. They are positioned more as infrastructure for AI workloads (NET) or as deep-vertical workflow software with proprietary data (PEGA) — both harder to displace with a horizontal agent than a flat per-seat productivity SaaS. Palantir (PLTR) sits just outside this group, with only a 3.4% holder drop versus double-digit losses for direct software peers — institutions appear to treat it as a distribution layer for AI rather than something AI is coming to replace.

The semi losers tell a different story — and a useful one for understanding what the sector trade is really about. Qualcomm (QCOM) lost 280 holders, more than any other chipmaker. Qualcomm sells almost entirely into smartphones and is exposed to Apple's modem displacement timeline — it is a semiconductor company by classification but not by the cycle the sector trade is actually buying. Broadcom and Nvidia losing holders is the more surprising signal: even AI's two biggest beneficiaries saw mild trims, suggesting some institutions are taking profits at the top of the position rather than walking away from the thesis. The smaller names — Impinj (PI), CEVA, Credo Technology (CRDO) — sit outside the data-center AI build, which appears to be where the bid actually concentrated.

Explore Ownership ChangesNotes

Holder data is drawn from SEC 13F filings comparing Q1 2026 (March 31, 2026) to Q4 2025 (December 31, 2025), covering the period after Anthropic's Claude Cowork launch in early February. Fund flow figures are from N-PORT filings; the most recent reported quarter varies by issuer (December 31, 2025 for IGV, SMH, SOXX, SKYY, CIBR; February 28, 2026 for the Fidelity portfolios; March 31, 2026 for First Trust Cloud Computing). The outlier chart excludes the pending Skyworks-Qorvo merger and the rumored Microsoft acquisition of Asana, since holder changes around announced deals are largely mechanical. See Trends for the full underlying data, and Screener to filter active managers by their software and semi exposure.