The Closed-End Fund Raiders: Inside Saba's 28-Fund Campaign

Most activist campaigns aim at a company — its board, its strategy, its costs. A smaller, busier kind of campaign aims at something more abstract: the gap between what a fund is worth and what its shares trade for. One firm has built much of its business around closing that gap, fund by fund — and because it also reports a quarterly portfolio, the campaign can be seen from both sides at once.

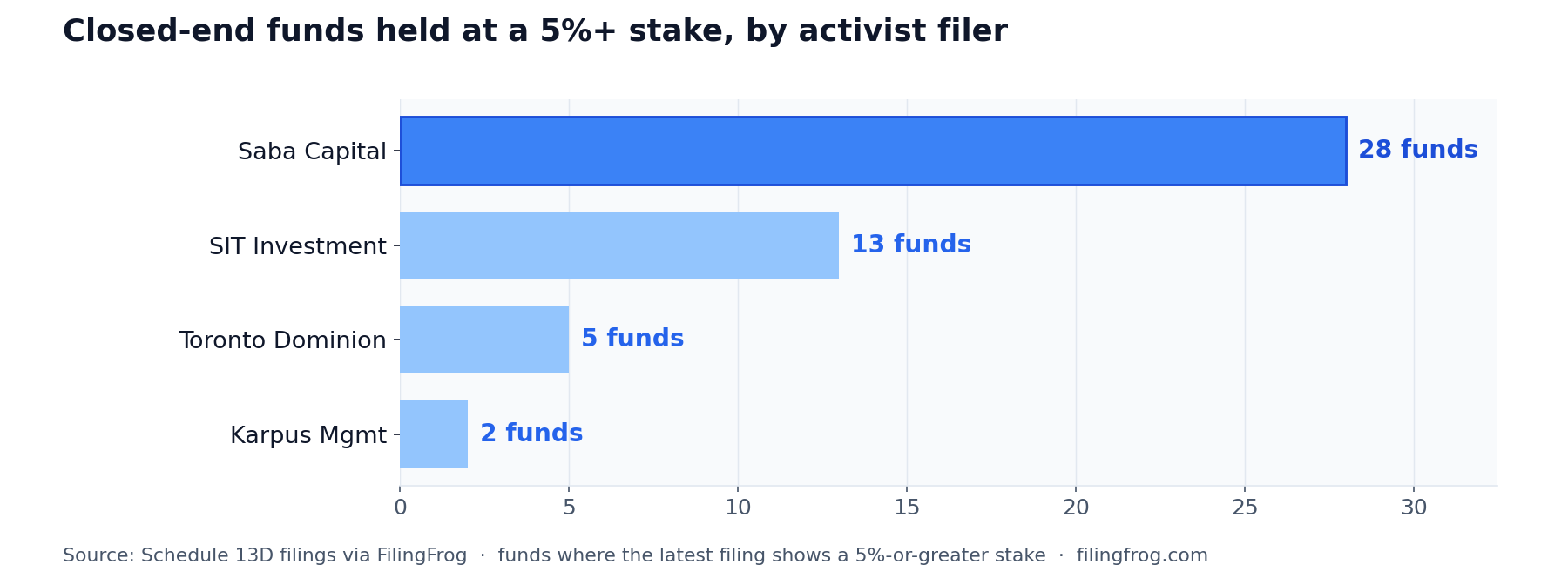

Schedule 13D filings over the past year show Boaz Weinstein's Saba Capital currently holding 5%-or-greater stakes in 28 closed-end funds, from about 5% to nearly 32% of a fund's shares — part of a rotation through more than 60 funds over time. By filing count it is one of the most active campaigners in the market — and, as its own portfolio shows, it owns what it agitates.

Saba's map

Closed-end funds raise a fixed pool of capital and then trade on an exchange, which means their share price can drift below the value of what they hold — a discount to net asset value. Saba's strategy is to buy into that discount across dozens of funds at once and press each one to close it. Its largest disclosed positions span gold, foreign equity, health sciences and multi-strategy income:

- ASA Gold and Precious Metals (ASA) — 31.9%

- Destra Multi-Alternative Fund (DMA) — 24.9%

- The New Germany Fund (GF) — 22.0%

- BlackRock Health Sciences Term Trust (BMEZ) — 20.0%

- BlackRock ESG Capital Allocation Term Trust (ECAT) — 19.1%

The portfolio underneath says the same thing

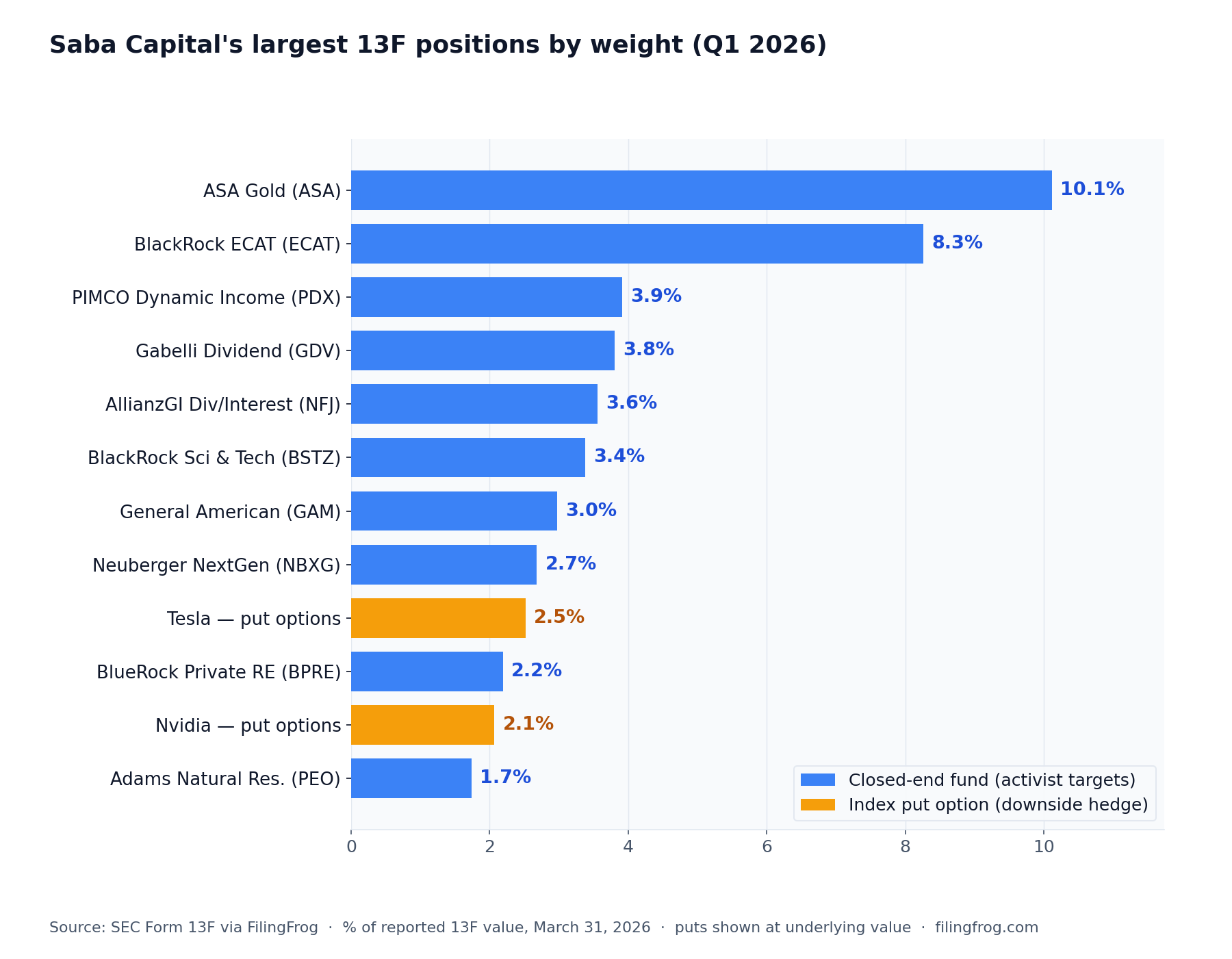

There is a second way to look at any manager: the quarterly Form 13F that lists what it actually holds. Saba's most recent one covers about $3.6 billion across 371 positions — and the top of that book is no surprise. Its two largest holdings by weight are the very funds it is campaigning against: ASA Gold at roughly 10% of the portfolio, and BlackRock's ECAT at about 8%. Below them the leaderboard keeps reading like the target list — Gabelli, AllianzGI, General American, Neuberger. The filings and the portfolio are the same idea seen through two different forms.

The whole portfolio, with its quarter-by-quarter history, sits on Saba's manager page — each holding clickable through to who else owns it.

A hedge book runs underneath

One thing the portfolio shows that the campaign filings don't: tucked among the closed-end funds sit a row of index put options — downside positions on Tesla, Nvidia, Meta and Boeing, together a meaningful slice of the book. That overlay is a long-running signature of Weinstein's, who built his reputation on tail-risk and volatility trades. Laid side by side in one filing, it is two strategies at once — the patient discount-closing book on one hand, a macro hedge on the other.

What moved last quarter

The quarter-over-quarter changes track the strategy in motion. Saba trimmed its ECAT position by about a third — from roughly 12% of the book to 8% — and stepped out of several smaller municipal funds. On the other side, it opened a new position in FS KKR Capital (FSK), a business development company, and added to its index put hedges. The move into a BDC lines up with Saba's stated push this year to carry the same discount playbook beyond listed funds into business development companies and interval funds.

The playbook, and a setback

The mechanics are consistent: accumulate, then push for a tender offer near net asset value, a buyback, or a board change that hands shareholders the discount in cash. In early 2026 Saba widened the aperture, launching tender offers for stakes in several Blue Owl semi-liquid private-credit vehicles at implied discounts of 20% to 35%. The strategy did meet a wall: on June 11, 2026, the Supreme Court ruled in FS Credit Opportunities Corp. v. Saba Capital Master Fund that a provision of the Investment Company Act does not create a private right of action to challenge fund governance measures — removing one of the legal tools activists had leaned on. The discounts, though, have not gone anywhere.

Not just Saba

The same trade supports a small cottage industry. SIT Investment Associates holds 5%-or-greater positions in 13 funds, mostly municipal and income vehicles; Toronto Dominion in five; and long-time discount hunters Karpus Management and Bulldog Investors round out the field. Different houses, same quarry: the persistent space between a fund's price and the value of what it owns.

Explore Saba's Full PortfolioNotes

Stake percentages and fund counts are drawn from Schedule 13D filings and amendments over the trailing twelve months through June 2026; each percentage reflects the filer's most recent disclosure for that fund. Portfolio weights and quarter-over-quarter changes are from Saba Capital's Form 13F for the quarter ended March 31, 2026, and are measured as a share of total reported 13F value — which lags the activist filings by a quarter. Saba's full holdings and history are on its manager page; the campaign filings are in the activist section.