Where Institutional Options Bets Actually Sit in Q1

Institutional managers reported close to $4.7 trillion in option notional on their latest 13F filings — roughly double what they reported three years ago. The bulk of that growth came from option market makers and prime-broker desks running balanced books, which is dealer plumbing rather than positioning. Pull those out and a few specific things stand out: put hedges on a single credit ETF that run more than 2.5× the fund's own size, an all-call book at one large-cap focused hedge fund, and a small set of long-equity managers carrying unusually heavy puts.

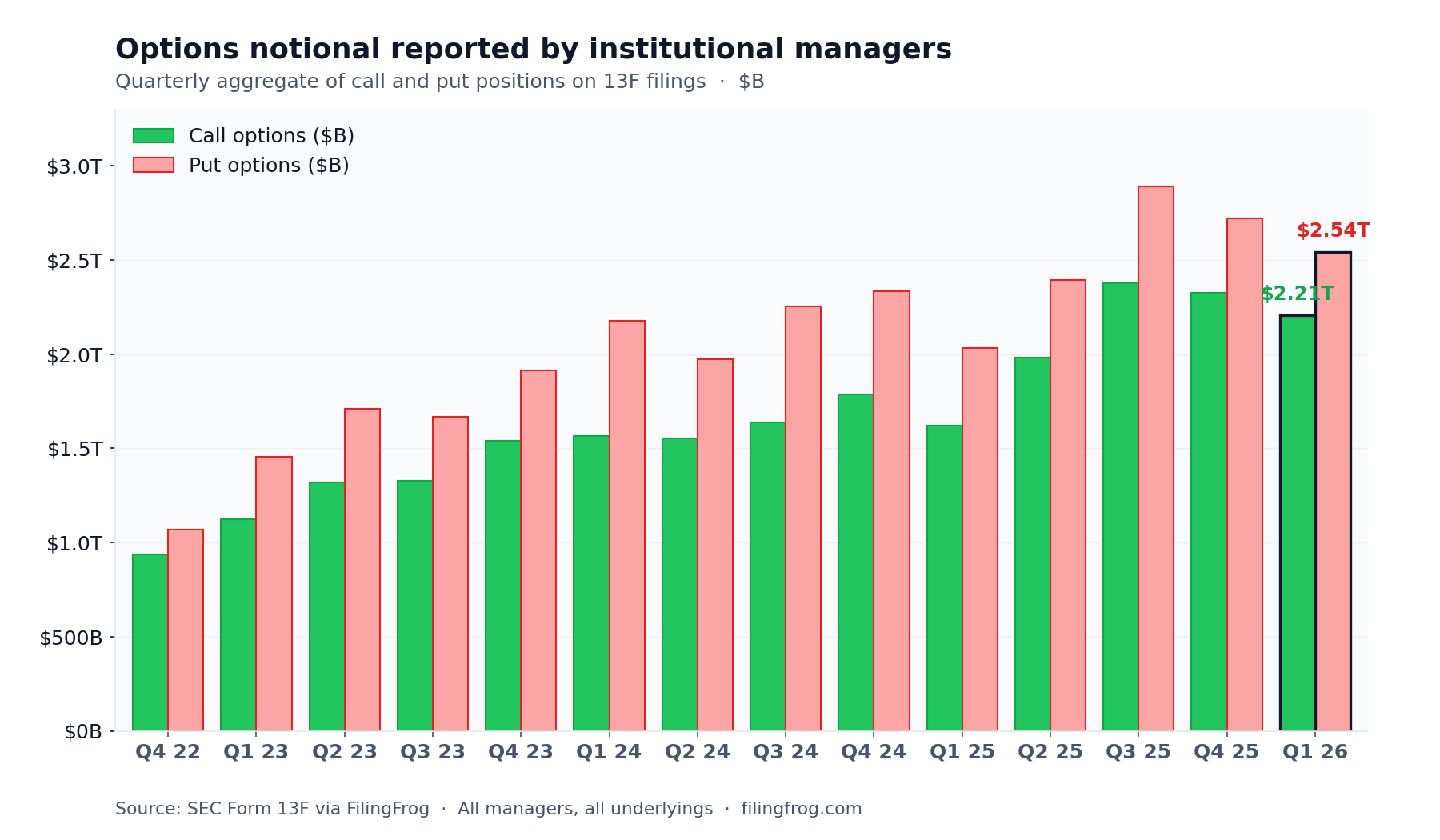

Notional has roughly doubled in three years

Call positions across all 13F filers rose from $936B in Q4 2022 to $2.21T in Q1 2026. Puts grew on a similar arc, from $1.07T to $2.54T. The two moved together — the put-over-call mix has stayed in a narrow band, roughly 53–55% puts in notional terms every quarter since 2022.

A large share of that growth sits at firms whose business is to be on both sides of a trade — option market makers like Susquehanna, Jane Street, Optiver and IMC, along with prime-broker option desks at the major banks. Their books are big and they grew with overall listed options volume, but the put and call totals are close to balanced because they are facilitating flow rather than expressing a view. For an investor reading 13Fs, those are the lines worth scrolling past.

The interesting lines sit elsewhere — in how the broad ETF puts pile up against the size of the actual funds, in where single-stock skew leans one way, and in a handful of managers whose option books look like positioning rather than market-making.

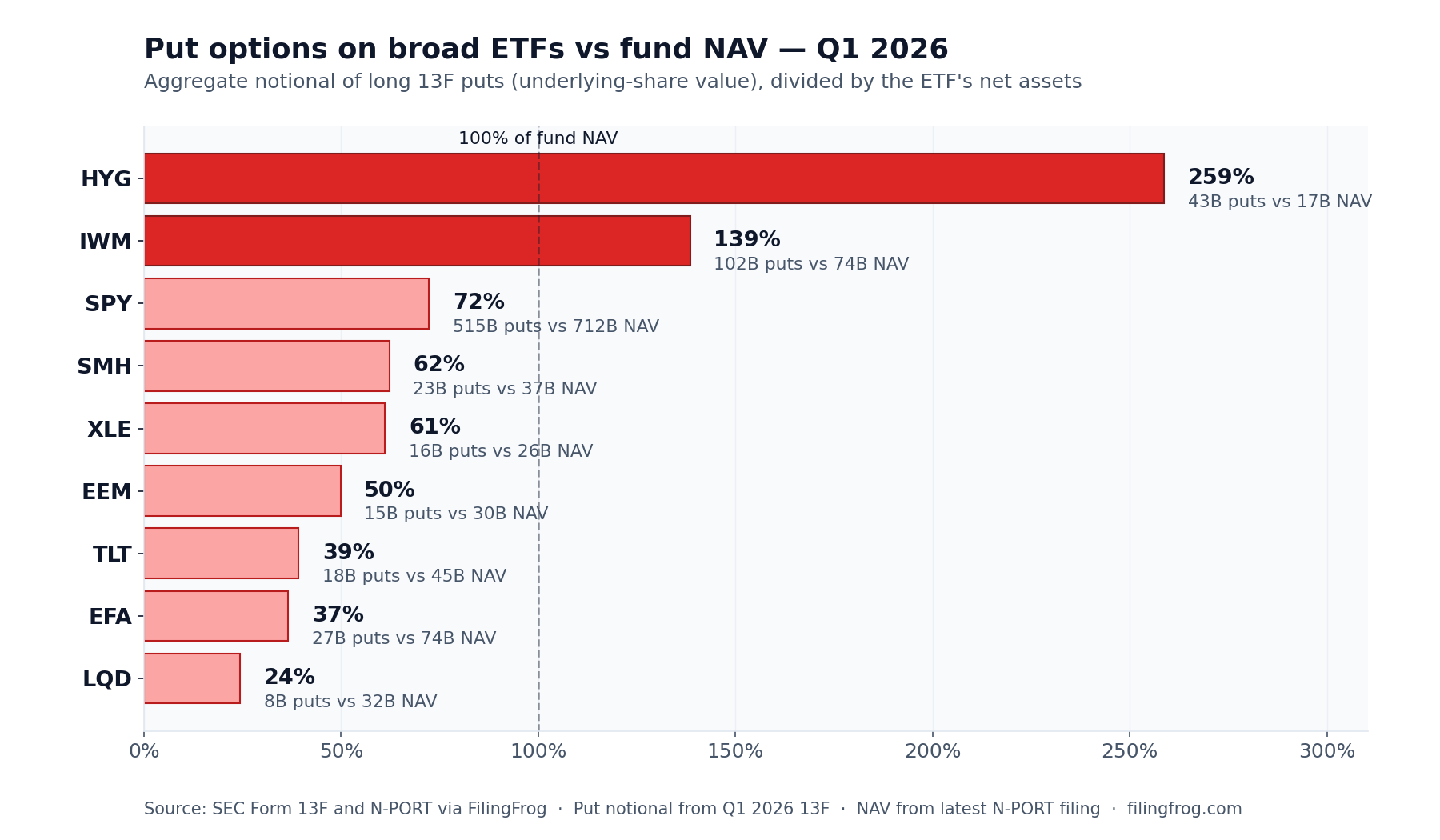

Put options on broad ETFs, sized against the ETFs themselves

When 13F filings show large put positions on tickers like iShares iBoxx \$ High Yield Corporate Bond ETF (HYG) or SPDR S&P 500 ETF Trust (SPY), the puts are options on the ETF itself, not on the underlying holdings. A manager who buys an HYG put is buying protection against the price of HYG — usually as a hedge against a portfolio of corporate credit. The size of those puts becomes interesting when measured against the size of the fund they sit on.

The chart compares Q1 2026 put notional on each ETF to the ETF's most recently reported net assets. Two stand out:

- iShares iBoxx \$ High Yield Corporate Bond ETF (HYG) — $43.2B in put notional against a $16.7B fund. Institutional put exposure is roughly 2.6× the size of the fund itself, the largest such gap on the list. HYG is the most-used vehicle for hedging high-yield credit, and the asymmetry has widened over the last year as credit spreads stayed tight.

- iShares Russell 2000 ETF (IWM) — $102B in put notional against a $74B fund. Small caps are the second-largest hedge book by ratio, well above large-cap and international ETFs.

On the mega-cap side, SPDR S&P 500 ETF Trust (SPY) carries the largest absolute put notional of any underlying anywhere — $515B across 380 distinct filers — but at 72% of the fund's $712B in net assets, the ratio is smaller than HYG or IWM. VanEck Semiconductor ETF (SMH) sits at 62% of NAV, in line with single-name semiconductor puts (more on this below). Treasury and investment-grade credit ETFs (iShares 20+ Year Treasury Bond ETF (TLT), iShares iBoxx \$ Investment Grade Corporate Bond ETF (LQD)) carry far less.

Single names lean the other way for mega-cap tech

At the single-stock level the skew often inverts. The largest call-tilted books sit on mega-cap technology and a handful of commodity proxies:

- Microsoft (MSFT) — 70% calls ($99.0B vs $42.1B puts), the most call-heavy mix of any large single-stock option book

- Meta Platforms (META) — 61% calls ($68.1B vs $44.0B puts)

- SPDR Gold Trust (GLD) — 54% calls ($87.3B vs $74.8B puts) — physical-gold trust

- Tesla (TSLA) — 53% calls ($91.1B vs $80.3B puts)

- Amazon (AMZN) — 54% calls ($44.2B vs $37.0B puts)

The semiconductor complex sits on the opposite side, with put notional running 50–60% larger than call notional across nearly every major name:

- Micron Technology (MU) — 60% puts ($40.7B vs $27.4B calls)

- Advanced Micro Devices (AMD) — 60% puts ($32.3B vs $21.4B calls)

- Broadcom (AVGO) — 60% puts ($30.1B vs $20.4B calls)

- Oracle (ORCL) — 58% puts ($17.1B vs $12.2B calls)

- Taiwan Semiconductor (TSM) — 55% puts ($27.4B vs $22.0B calls)

NVIDIA (NVDA) sits roughly balanced at $108B puts against $97B calls, with more than 220 filers on each side. The book is the largest of any single name by absolute notional, but the holder breadth on both sides is closer to an index than a single position.

A few managers carry one-sided option books

Most multi-strategy funds run option books that look balanced — Citadel, Millennium, D.E. Shaw, Tudor, Balyasny and Squarepoint all sit close to a 50/50 put-to-call split, which is what hedging-driven flow tends to look like. A smaller set of managers stand apart with books that are markedly tilted one way:

- Soroban Capital Partners — $37.8B in calls and no reported puts. The book is concentrated on three names: $22.2B Microsoft calls, $11.4B Meta calls, $4.2B Amazon calls. Combined with the firm's equity longs in the same names, that is a single fund pressing a concentrated bullish AI-mega-cap view at scale.

- Capstone Investment Advisors — $34.9B puts vs $10.4B calls (77% puts), anchored by $10B in SPY puts and $9.7B in QQQ puts. Capstone's stated business is volatility, so a put-heavy book is structural rather than directional, but the scale of the index puts is worth noticing.

- LMR Partners — $29.7B puts vs $4.8B calls (86% puts). A macro multi-strat with the option line tilted hard defensive.

- 1832 Asset Management — $28.1B puts vs $5.2B calls (85% puts), with options at roughly 31% of disclosed assets.

- Alkeon Capital Management — $27.4B puts vs $10.0B calls (73% puts). A long-biased growth equity manager running a sizable hedge against its own book — unusual for the style, and the kind of mix worth watching across quarters.

A 13F filing only shows long option positions at quarter end. It does not disclose strikes, expiries, or whether the position was bought or written, and it does not show short option positions or short stock against them. A long-call line could be a directional bet or a covered-call program; a long-put line could be a portfolio hedge or a short bet. The signal that does survive is participation breadth and relative skew — and where those line up unusually, the disclosure is at least pointing at something.

Browse Manager PositionsNotes

Options aggregates are computed from 13F holdings filed for the periods ending December 31, 2022 through March 31, 2026. Q1 2026 numbers reflect filings received through mid-May 2026. For options, the 13F value field reports the market value of the underlying shares the contracts cover, not the option premium itself — so the put notionals above reflect underlying-share exposure rather than hedge-premium dollars, and strike and delta are unknown. 13F filings also do not separate purchased from written positions, do not disclose strikes or expirations, and do not report short option positions or short stock. ETF net assets are sourced from each fund's most recent N-PORT filing. Individual manager option books can be inspected on each manager page, and ticker-level option holders are visible on each security page (e.g. HYG, MSFT).