Q1 2026 13F Update: What 1,300 Filers Show at 15% Coverage

The first look at Q1 2026 filings covered 193 managers who reported in the opening days of April — a sample dominated by smaller RIAs. Two weeks later, roughly 1,300 managers have filed their March 31 holdings. That's about 15% of the managers who reported for Q4 2025, and it's still skewed toward mid-sized and international firms. The largest U.S. asset managers typically file in the final week before the May 15 deadline, so these signals could shift materially as the rest of the universe comes in.

All manager-count comparisons below use an apples-to-apples cohort: for each security, the figures compare how many of these same 1,300 managers held it in Q4 2025 versus Q1 2026. Managers who filed Q1 but didn't hold a name in Q4 count as new buyers; those who held in Q4 but dropped in Q1 count as sellers. No Q4-only managers are included in the denominator, so the percentages reflect actual portfolio decisions within this cohort — not a comparison against the full Q4 universe.

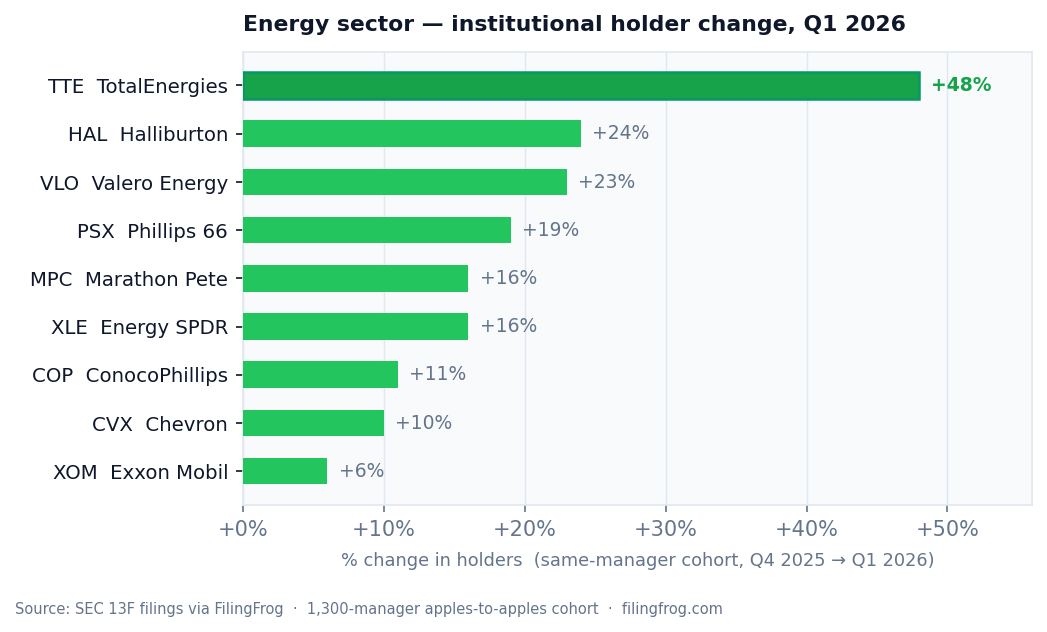

Energy: a broadly held call, not just a tilt

The early-filer energy signal from the first article has held and widened. Every major segment — integrated majors, refiners, oilfield services, international producers, and the broad energy ETF — saw more of this cohort hold it in Q1 than in Q4. TotalEnergies (TTE) led on percentage change: 48% more of the cohort held it in Q1. Refiners were the next strongest: Valero Energy (VLO) and Phillips 66 (PSX) each added holders among roughly 20% of the cohort. Exxon Mobil (XOM), already the most widely held energy name with 863 prior-period holders, added 6% — smaller percentage but meaningful at that scale.

Refiners — Valero (VLO), Phillips 66 (PSX), Marathon Petroleum (MPC) — saw position values rise 45–57% alongside the holder count increases, reflecting both new entry and Q1 margin widening as crude spreads shifted. The Energy Select Sector SPDR (XLE) gaining 16% more holders suggests some of this is managers reaching for broad sector exposure rather than picking individual names.

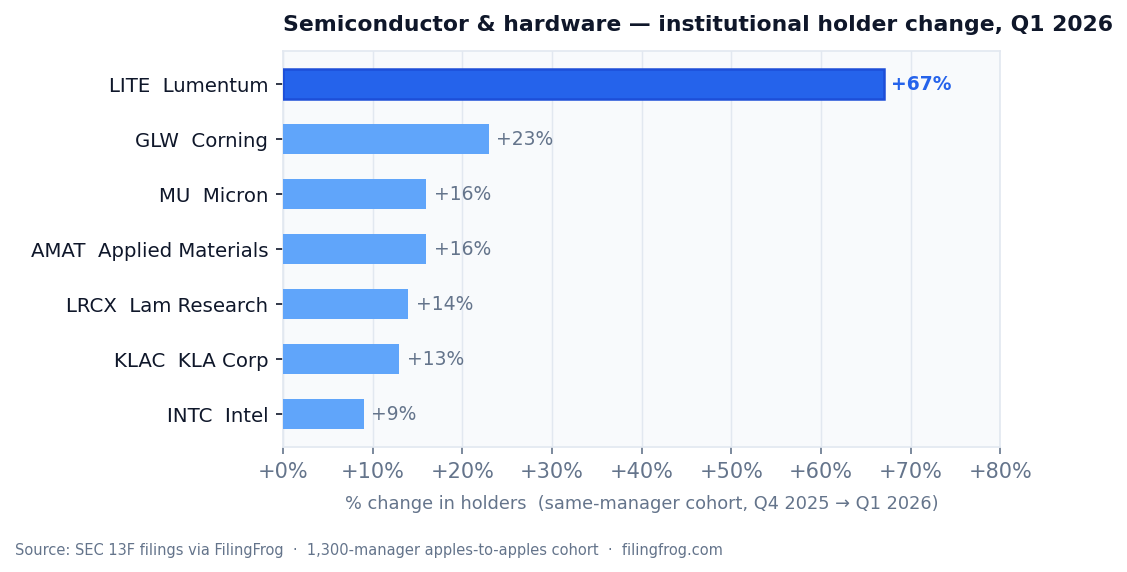

A semiconductor equipment cluster that wasn't visible at 193 filers

With 193 early filers this pattern was too thin to read. At 1,300 it's consistent enough to flag. Applied Materials (AMAT), Corning (GLW), Micron Technology (MU), Lam Research (LRCX), KLA (KLAC), and Intel (INTC) all added holders within this cohort — each up 9–23%. Lumentum Holdings (LITE) was the standout at +67%, the largest percentage increase of any widely held name in the dataset, with the company projecting to cross $600M in quarterly revenue by mid-2026 on AI data center optics demand.

The buying is concentrated in equipment and materials names rather than chip designers. Nvidia (NVDA) and AMD both saw near-zero net holder change within this cohort. Whether this reflects a view on AI capex durability, a rotation into value within semiconductors, or simply different holding patterns among the mid-sized managers who file early is difficult to determine from the filings alone.

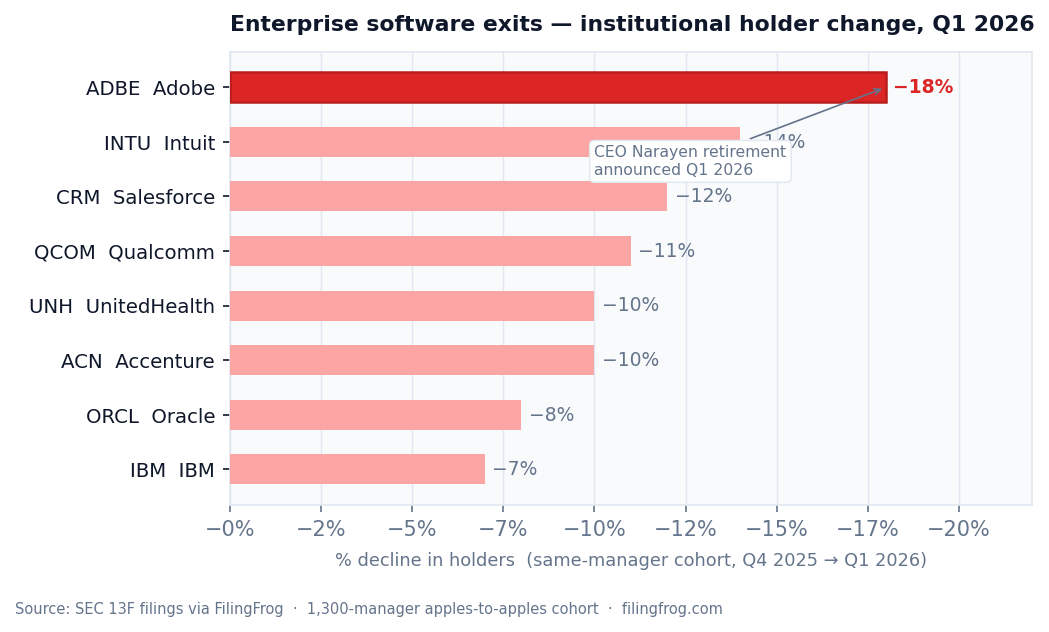

Enterprise software takes the exit, not the hyperscalers

The first article noted broad selling of growth and tech positions. With more data, the pattern sharpens. Adobe (ADBE) lost holders among 18% of the cohort — the largest decline of any widely held name in the dataset. CEO Shantanu Narayen, who had led Adobe for 18 years, announced his retirement during Q1 2026. Leadership transitions of that length tend to create uncertainty about strategic direction, particularly for a company navigating an AI disruption to its core creative software business. Intuit (INTU), Salesforce (CRM), Qualcomm (QCOM), Oracle (ORCL), and IBM followed, each losing 7–14% of the cohort as holders.

The hyperscalers moved much less. Microsoft (MSFT) was essentially flat; Amazon (AMZN), Alphabet (GOOGL), and Meta (META) each lost holders among 1–3% of the cohort. The selling was specific to the second tier — enterprise SaaS, legacy IT services, and chip designers — not broad tech.

Infrastructure and defense added quietly

GE Vernova (GEV) added the largest nominal holder count of any name in the dataset: +77, or 16% more of the cohort. Worth noting: GEV was added to the S&P 100 on March 23, 2026 — one week before Q1 ended — which would have mechanically required index-tracking funds to initiate positions. Some portion of the +16% likely reflects that. The S&P 500 inclusion came later, on April 2, so that effect will show in Q2 data. Vertiv Holdings (VRT), which makes data center power equipment, added holders among 27% of the cohort with position values up 60% — no index event behind that move. Defense names added holders quietly: Lockheed Martin (LMT) up 9%, RTX up 4%, Northrop Grumman (NOC) up 7%.

- GE Vernova (GEV) — +16% of cohort as holders (partly S&P 100 inclusion effect), position values +36%

- Vertiv Holdings (VRT) — +27% of cohort as holders, position values +60%

- Lockheed Martin (LMT) — +9% of cohort as holders, position values +29%

- RTX Corporation (RTX) — +4% of cohort as holders

Some large holder-count drops are M&A completions, not exits

A handful of names show near-total holder collapses with mechanical explanations. Comerica (CMA), CyberArk Software (CYBR), Cadence Bancorp (CADE), and Dayforce (DAY) each went from 30–60+ cohort holders to essentially zero, with position values falling 99–100%. These are closed acquisitions — when a deal settles, every manager who held for the arbitrage exits simultaneously. Capital One Financial (COF) lost holders among 11% of the cohort with values down 49%, reflecting the resolution of the Capital One–Discover Financial deal that closed in February 2026. When deals close, that capital relocates; some of it may be visible in the energy and infrastructure buying above.

What comes next

The 1,300 managers who have filed represent roughly $1.1 trillion in reported U.S. equity holdings — about 1.6% of the $67.6 trillion reported across all managers in Q4 2025. The largest asset managers file late. When they arrive in the final days before May 15, the aggregate totals will change materially, and patterns visible in this early cohort may look different at scale. The semiconductor equipment cluster in particular bears watching — it either reflects a broadly held view or a characteristic of the mid-sized managers who happen to file early.

Explore Ownership ChangesNotes

Data covers 13F filings for Q1 2026 (period ending March 31, 2026) with filing dates through April 17, 2026 — approximately 1,319 managers. All manager-count changes compare each manager's March 31, 2026 holdings against their December 31, 2025 holdings within the same cohort; managers who filed Q4 but have not yet filed Q1 are excluded from both periods. Percentages are rounded to whole numbers. GE Vernova's S&P 100 inclusion became effective March 23, 2026; its S&P 500 inclusion took effect April 2, 2026. Adobe CEO Narayen retirement announcement was made during Q1 2026. Part 1 of this series is at Q1 2026: First Filings In. Full ownership history for individual securities is available through the ownership changes section.