SpaceX, OpenAI, and Anthropic Are Going Public — What Will They Actually Weigh in Your Index Funds?

SpaceX is pricing the largest IPO in history this week — about $1.77 trillion, ticker SPCX, set to begin trading on Nasdaq around June 12 — with OpenAI and Anthropic close behind, each having filed confidentially in the past two weeks at valuations near a trillion dollars of their own.

A lot of people are bracing for these three large, unprofitable companies to come flooding into their retirement accounts. The way index funds actually decide how much of a new stock to hold makes the real number much smaller than the headlines suggest — and surprisingly different depending on which fund you happen to own.

Index funds weight free float, not headlines

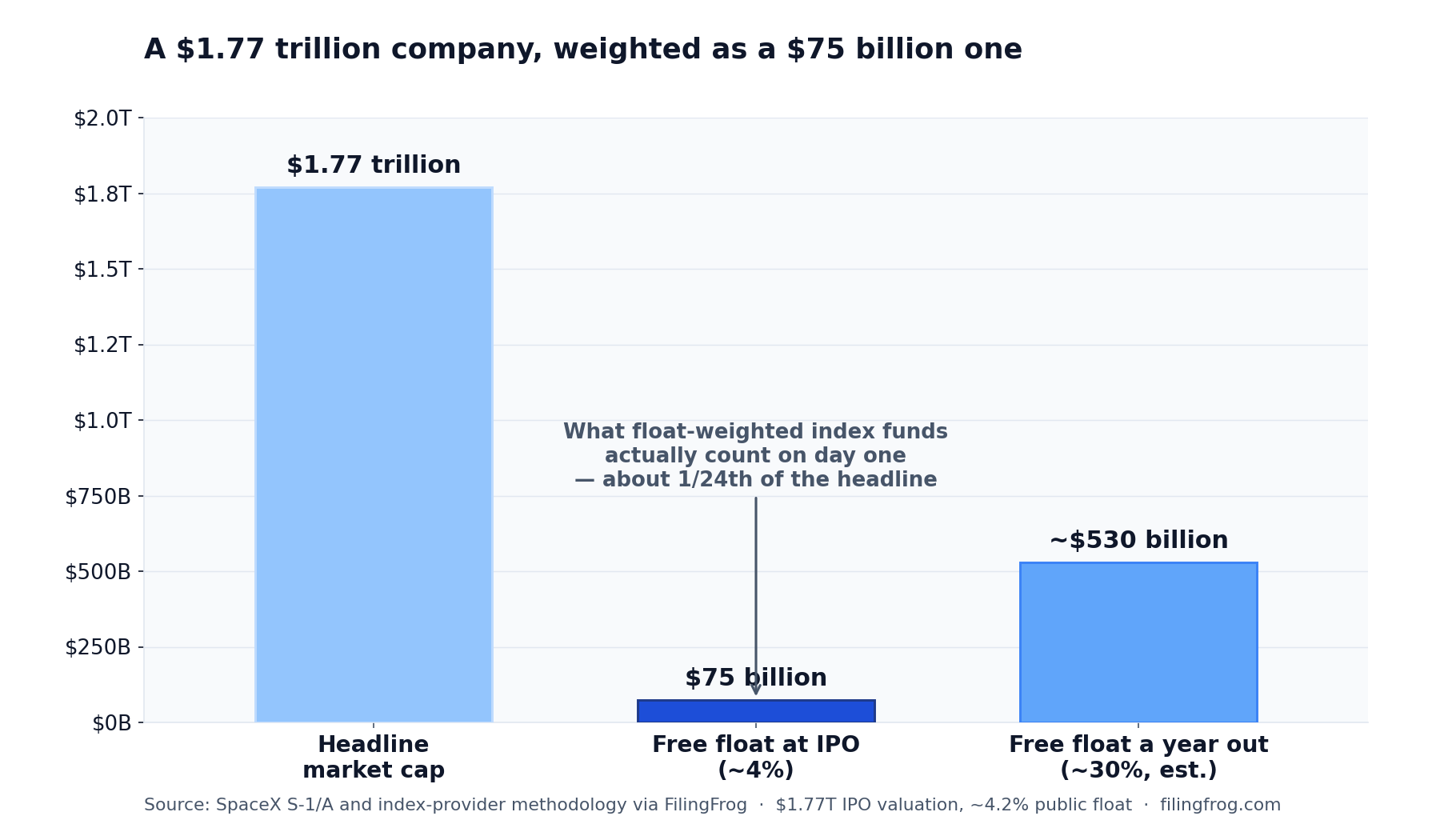

A cap-weighted index fund does not weight a company by its market value. It weights the slice of shares that actually trades freely — the public float. SpaceX is selling about 556 million shares, roughly $75 billion worth, out of some 13 billion shares outstanding. Only about 4% of the company will float at the listing.

So the $1.77 trillion headline is not the number that goes into an index. The float-adjusted figure — around $75 billion — is, which is about a twenty-fourth of the headline. A company that ranks as the seventh-largest in the United States by market value enters a float-weighted index looking, for weighting purposes, like a mid-sized one.

That float grows over time. SpaceX's lockups release in stages over roughly the first six months, so more shares become tradable as the year goes on. But the weight is permanently capped well below the headline: Elon Musk keeps about 42% of the economics — and 82.4% of the votes, through a second class of stock — and a founder's controlling stake never counts as float. The funds that end up holding SpaceX will own a company where their shareholder vote barely registers.

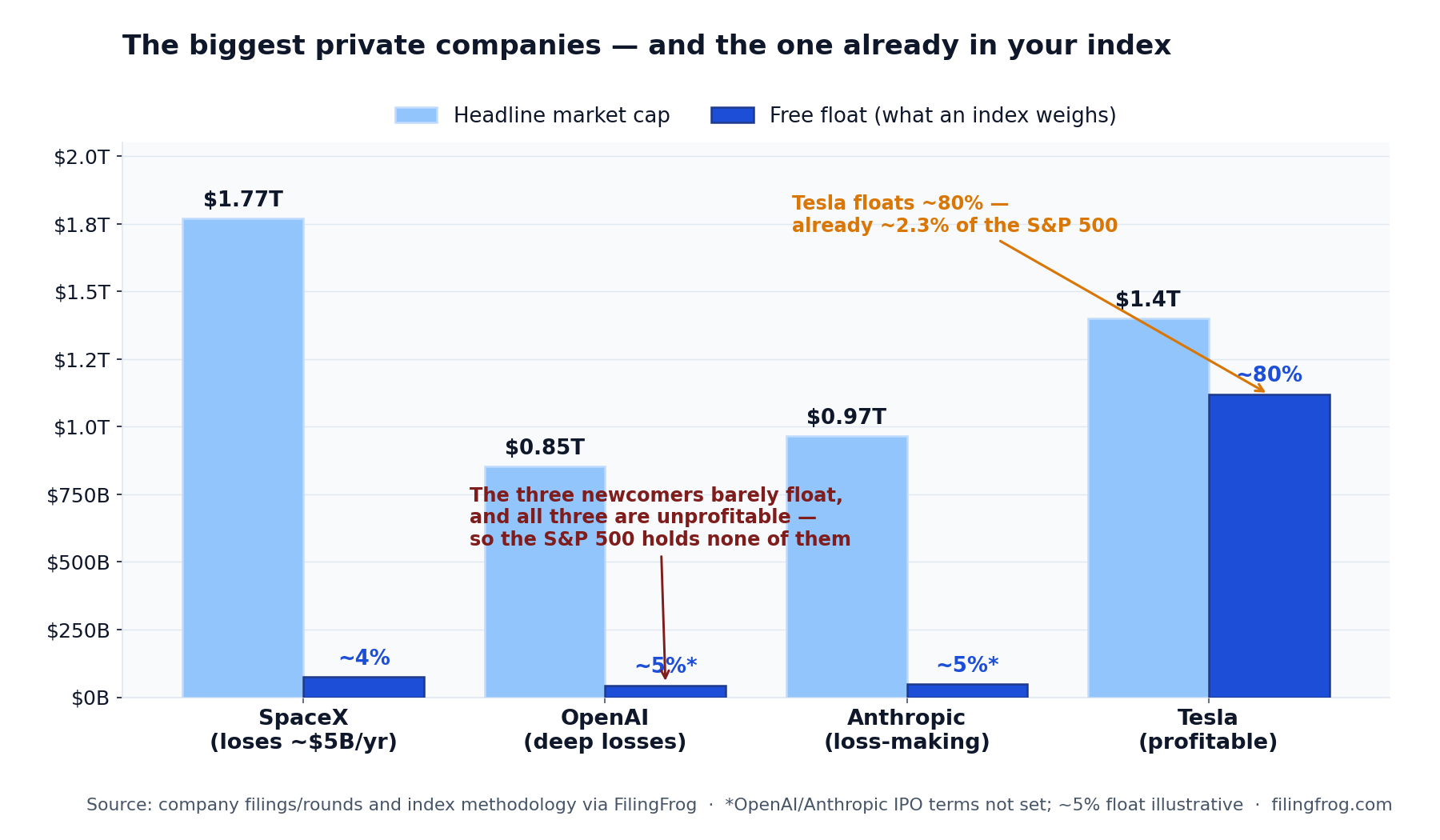

The other two are close behind — and lose more

SpaceX is the biggest of the three, but the other two are not far behind. Anthropic's late-May funding round valued it near $965 billion — the most valuable startup the AI boom has produced — and OpenAI's last round landed around $850 billion. The chart below lines all three up against Tesla (TSLA), a company already sitting in the index, and the three newcomers share a shape: an enormous headline valuation, a thin sliver of tradable stock, and losses underneath.

OpenAI is the deepest in the red, losing on the order of $12 billion in a single recent quarter even as its revenue climbed past a $25 billion annual pace; Microsoft owns about 27% of it. Anthropic is closer to break-even — its revenue run-rate has jumped from roughly $9 billion at the end of 2025 toward the mid-tens of billions this spring — but it still spends well ahead of what it earns, with Google and Amazon together holding roughly a third. Tesla is the outlier: it turns a profit, and about 80% of its shares trade freely, which is why it already makes up about 2.3% of the S&P 500 while these three are not in it at all. Their IPO floats are not set yet, but each is founder- and strategic-heavy, so a SpaceX-like sliver is the reasonable expectation.

The single most common index in a 401(k) won't hold any of them

The S&P 500 is the building block at the center of most retirement menus. It also has rules a brand-new, unprofitable, low-float company cannot meet: a 12-month trading history, a public float of at least 10%, and positive net income — under standard accounting — in both the latest quarter and the trailing year. SpaceX misses all three at once, and the other two miss the profitability test by even wider margins.

In April, S&P opened a consultation on whether to bend those rules for the wave of trillion-dollar IPOs. On June 4 it declined, keeping the seasoning period, the float minimum, and the profitability test in place — noting that exceptions "should not be granted solely based on market capitalization." So on the day SpaceX becomes one of the largest companies in the country, its weight in an S&P 500 fund is exactly zero, and it stays there until the company strings together profitable quarters — perhaps 2027 at the earliest, perhaps later. The block is not permanent; it lifts the moment earnings turn positive and stay there. But it is open-ended, not a date on a calendar, and the profitability test has no size waiver — being enormous does not help.

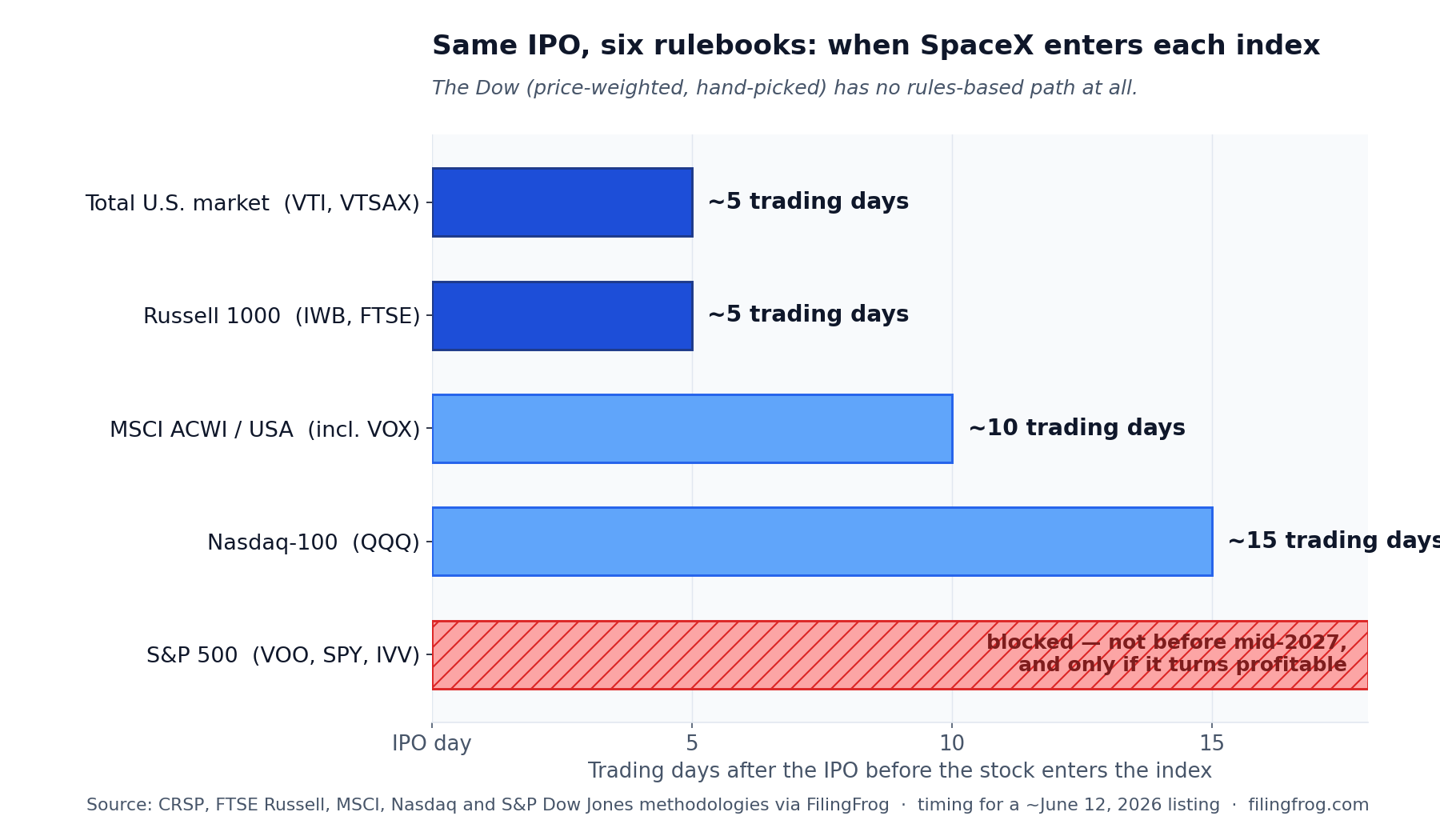

Some index families wave them in within days

While S&P held its line, other providers spent the spring rewriting theirs. The result is that the first place SpaceX shows up is not the S&P 500 at all — it is the broad total-market and Russell funds, which carry no profitability screen and added off-cycle fast-track rules this spring.

- Total U.S. market (VTI, VTSAX) — about 5 trading days after listing

- Russell 1000 (IWB) — about 5 trading days

- MSCI ACWI and USA (and the Vanguard sector funds built on MSCI) — about 10 trading days

- Nasdaq-100 (QQQ) — about 15 trading days

- S&P 500 (VOO, SPY, IVV) — blocked, likely not before mid-2027

Most savers hold some of this broad exposure without ever choosing it. Target-date funds — the default option in the majority of 401(k) plans — are usually built on total-market and Russell building blocks, which are exactly the ones that pick SpaceX up first. So the median saver probably does end up holding a little SpaceX within a few weeks of the IPO — just not through the S&P 500, and not very much. The same doors open for OpenAI and Anthropic when they list later this year: the total-market, Russell, MSCI and Nasdaq rules carry no profitability test, so those funds can take them in within days while the S&P 500 stays shut. Nasdaq's own overhaul, effective May 1 and finalized weeks before SpaceX chose to list there, scrapped its 10% float minimum and created a 15-day path for the largest new listings; some observers called it a rulebook written for one company.

What the weight actually works out to — at the open, and a year on

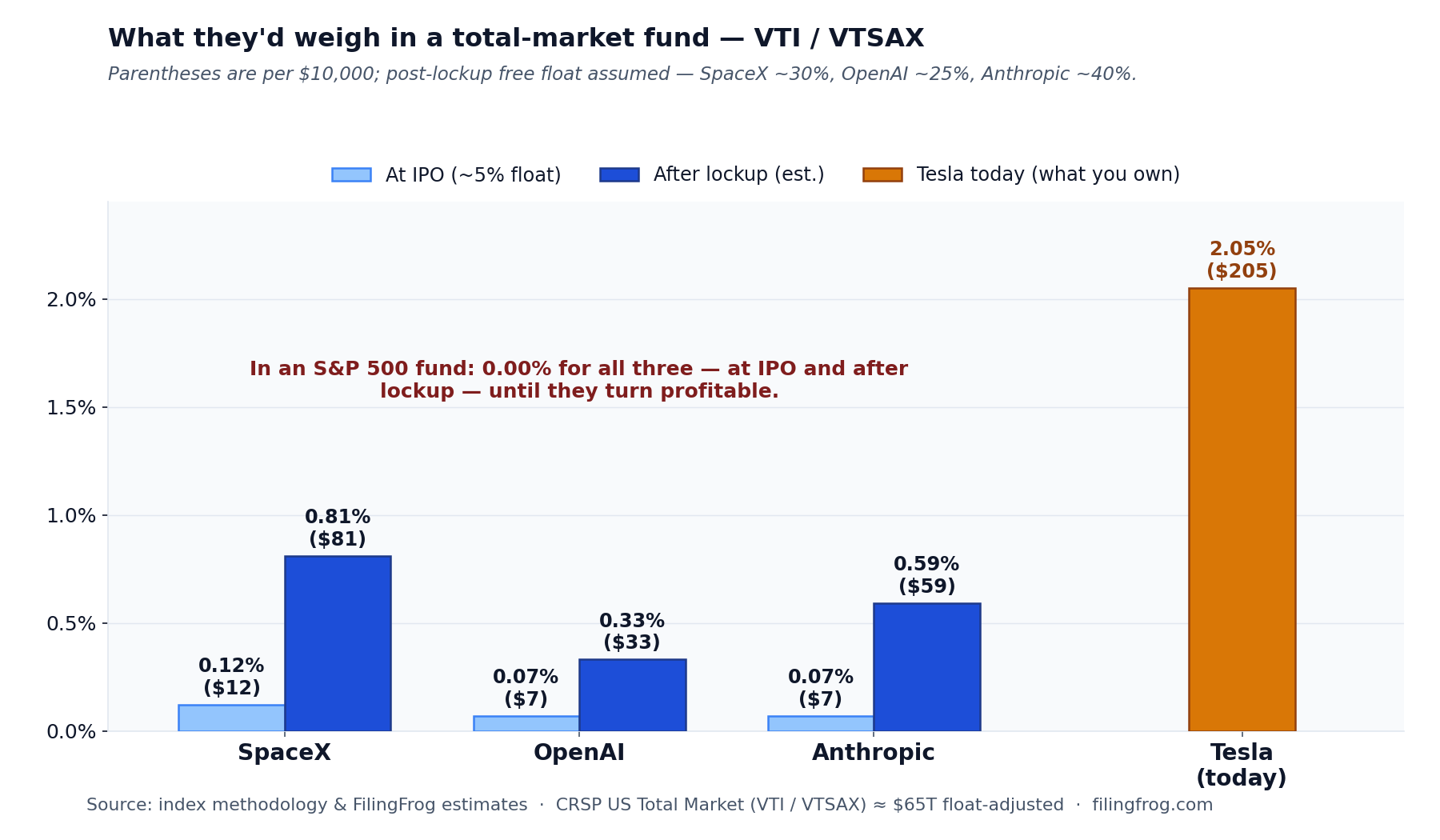

Put the float and the index sizes together and the numbers come out small. On its first days in a total-market fund like Vanguard's VTI or VTSAX — both of which track the CRSP US Total Market index — SpaceX would weigh about 0.12%, roughly $12 of SpaceX for every $10,000 invested. OpenAI and Anthropic, with less floated at the debut, would each land near 0.07%, about $7.

Where they settle after lockups depends on how much of each company will ever trade — and the three cap tables differ sharply. SpaceX has Musk's locked ~42%. OpenAI is the most closely held: Microsoft (~27%), the controlling OpenAI Foundation (~26%) and SoftBank (~12%) together own about two-thirds that will not change hands, leaving a thin public float. Anthropic is the most open of the three — Google, Amazon and the founders hold roughly 44%, but the rest is spread across dozens of financial investors who can sell. Translating each into free float — about 30% for SpaceX, 25% for OpenAI, 40% for Anthropic — gives the after-lockup weights below.

A year on, SpaceX would weigh about 0.8% of a total-market fund ($81 per $10,000), Anthropic about 0.59% ($59) and OpenAI about 0.33% ($33) — Anthropic nearly double OpenAI, not because it is much larger but because more of it trades. The reference bar is the point: Tesla — the example here, not one of the three — already sits near 2% of a total-market fund, about $205 of every $10,000, because roughly 80% of it floats. SpaceX still arrives about seventeen times lighter on its first day. And in an S&P 500 fund specifically, the figure is zero for all three, at the open and after lockup, until they turn profitable.

For scale, that same $10,000 in an S&P 500 fund already holds roughly $700 of Nvidia (NVDA) and $630 of Apple; the Magnificent Seven together make up about a third of the index. The "$20-to-30-billion of forced buying" quoted for this summer is real in aggregate, spread across trillions of dollars in index assets — but at the level of one account, it is the dollars above.

In the Nasdaq-100, the same math runs hot

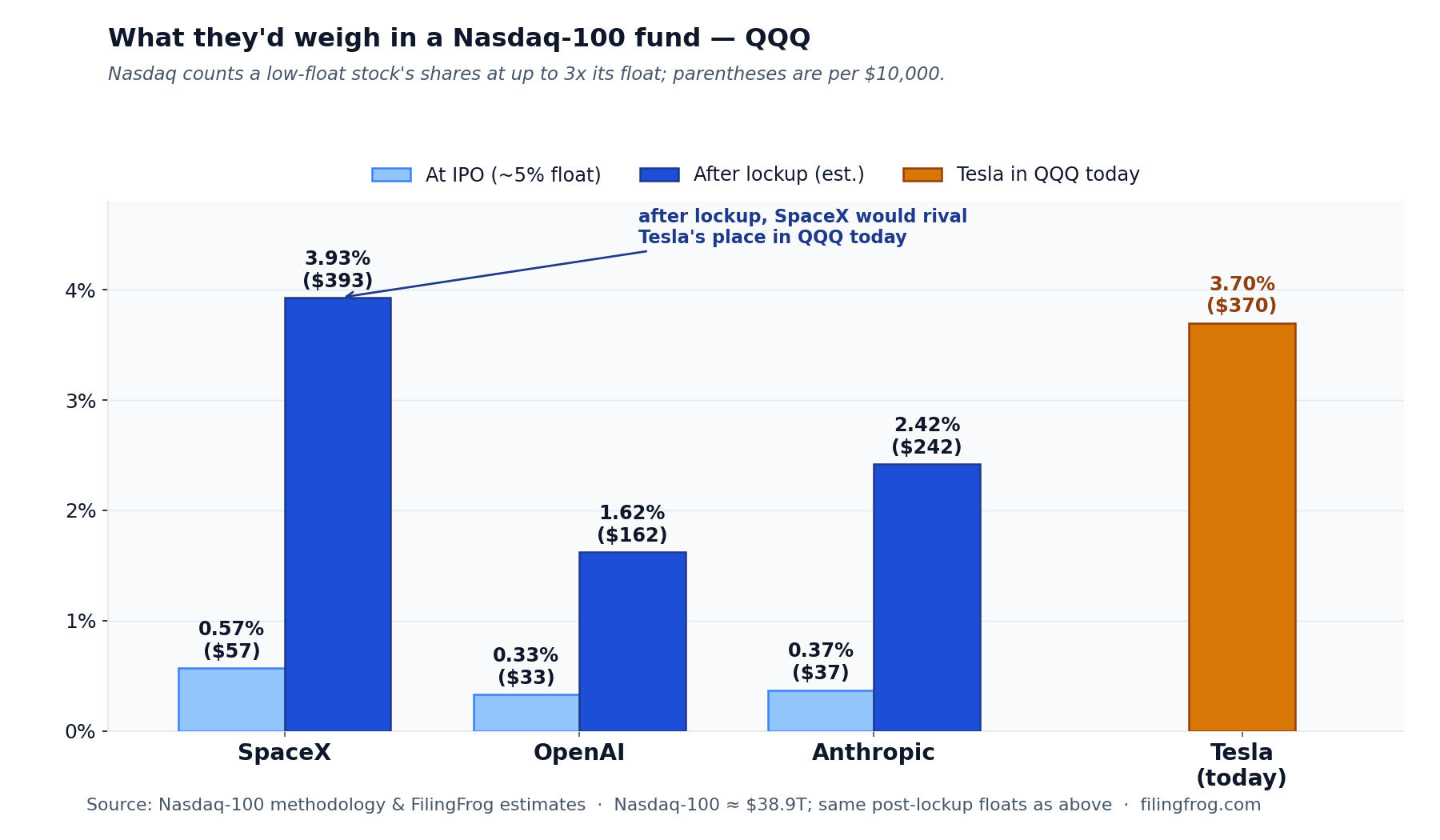

The Nasdaq-100 — the index behind QQQ — is the exception. It is smaller than the whole market (about $39 trillion), and under a rule Nasdaq adopted in May it counts a low-float stock's shares at up to three times their actual float. Both forces push the weights up.

At the open, SpaceX would be about 0.57% of QQQ — roughly $57 per $10,000, already five times its total-market weight. After lockups the gross-up bites harder: at a ~30% float, Nasdaq would count SpaceX at about 90% of its full value, lifting it to nearly 4% of QQQ — about $393 per $10,000, within range of where Tesla sits in the fund today. Anthropic would reach about 2.4% and OpenAI about 1.6%. The saver who holds QQQ rather than a total-market fund ends up with several times the exposure to the same three companies — not because they own more of them, but because of how the index counts low-float shares.

In the sector funds it gets lopsided — and SpaceX could go two ways

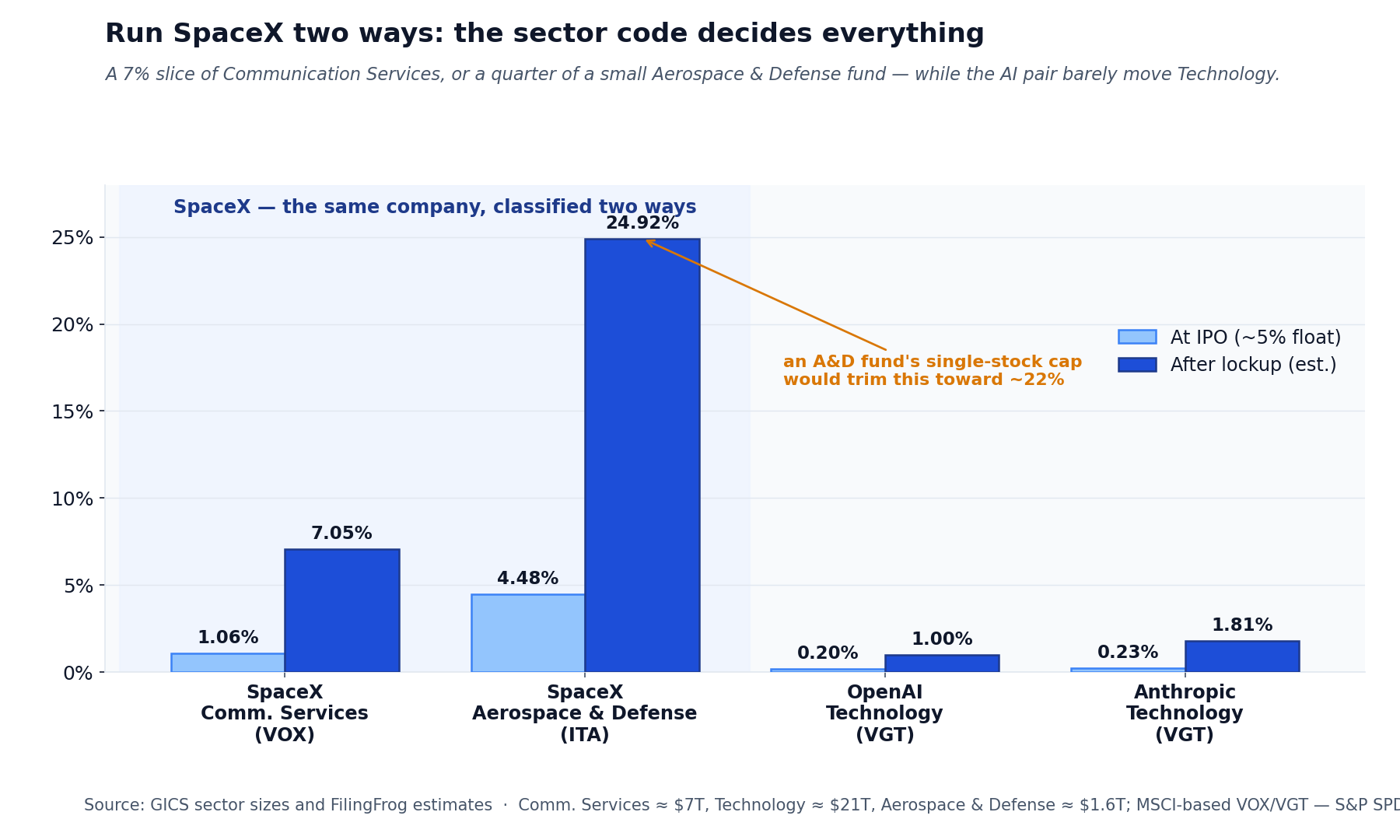

SpaceX's sector is not settled. Starlink is about 61% of revenue and nearly all of the profit, which points to Communication Services — alongside Alphabet, Meta and Netflix. But the rockets and launch business fit Aerospace & Defense, and the index providers had not made the call as of early June. The choice matters enormously, because the two pools are wildly different sizes.

In a communication-services fund, SpaceX would be a meaningful but not dominant holding — about 1% at the open, climbing toward 7% (roughly $700 of every $10,000) as its float widens. Drop the very same company into an aerospace-and-defense fund, a far smaller pool of around $1.6 trillion, and it would tower: close to 5% at the open and nearly a quarter of the fund after lockup — so large that the index's single-stock cap, near 22%, would have to rein it in. One classification decision is the difference between a top-ten name and the biggest position in the fund.

OpenAI and Anthropic point toward Technology, the largest sector of all, so they barely move it: on the order of 0.2% at the open and 1% to 1.8% after lockup. The same company can be a rounding line in one fund and a dominant weight in another.

One detail decides which sector funds are touched at all. The funds built on MSCI indexes — Vanguard's VOX for communication services, VGT for technology — carry no profitability screen, so they could add these names within weeks of listing. The sector funds carved out of the S&P 500 — the Select Sector SPDRs like XLK, XLC and the industrials XLI — inherit the index's profitability gate, so they hold none of the three until the S&P 500 does. And among the dedicated aerospace funds, the ones that screen by sector code (ITA, XAR) only pick SpaceX up if it is classified there in the first place; an activity-based one like Invesco's PPA, which explicitly covers government space operations, could hold it either way.

If you want more of this — or less

For someone who would rather not own unprofitable mega-caps, the S&P 500 already does the screening, and quality-tilted funds (QUAL), equal-weight (RSP), value and dividend funds lean further away from them. The products that pick these names up fastest are the broad total-market and Nasdaq-100 funds.

For someone who wants in before the lockups lift, the vehicles already exist — and they already hold these companies as private positions. The exchange-listed Destiny Tech100 (DXYZ) carries SpaceX at around 16% of the fund; ARK's venture fund holds all three; Baron and Coatue funds carry large private stakes. We mapped which funds hold the most of each, by weight, in a companion piece on fund exposure, and each company's cross-fund view is linked in the notes below.

Explore Fund HoldingsNotes

Figures are drawn from SpaceX's S-1/A registration statement, the published methodologies of S&P Dow Jones Indices, CRSP, FTSE Russell, MSCI and Nasdaq, the reported cap tables of all three companies, and reporting on the June 2026 IPO wave. SpaceX terms reflect the roadshow target of $1.77 trillion at $135 per share with about 4% of shares offered; the implied share count and float percentage are computed from those figures and will shift at final pricing (Morningstar's independent fair value is roughly $780 billion). OpenAI (about $850 billion) and Anthropic (about $965 billion) are private, file no audited financial statements, and have not set IPO terms — so their valuations are private-round marks, their loss figures are estimates, and the ~5% IPO floats shown for them are illustrative.

Index weights and the per-$10,000 figures are estimates: each company's float-adjusted market value divided by the relevant index total (total U.S. market ≈ $65 trillion; Nasdaq-100 ≈ $38.9 trillion; Technology sector ≈ $21 trillion; Communication Services ≈ $7 trillion; Aerospace & Defense ≈ $1.6 trillion). The Nasdaq-100 additionally counts a low-float stock's shares at up to three times its free float, which lifts its weights well above a total-market fund's. The "after lockup" weights turn on a free-float estimate for each company, since index funds weight only the shares that trade and exclude large strategic and insider blocks. The reasoning, drawn from each cap table:

- SpaceX — about 30%. Elon Musk holds roughly 42% of the equity and is locked for a year, and other insiders hold a further large block; free float is bounded under ~58% and realistically lands near 30% in the first year as the staged lockups release.

- OpenAI — about 25%. Microsoft (~27%), the controlling OpenAI Foundation (~26%) and SoftBank (~12%) together hold about two-thirds that does not trade; the public float is essentially the employee stake (~25%) as it unlocks.

- Anthropic — about 40%. Google (~14%), Amazon (mid-teens) and the founders are strategic — roughly 44% in all — but the remaining majority is spread across dozens of financial investors with no dominant block, so more of it floats once lockups lift.

These floats are estimates, not disclosures, and the resulting weights move with price and with how much locked stock is actually sold. Tesla figures (about 80% float; ~2% of a total-market fund, ~2.3% of the S&P 500, and ~3.7% of the Nasdaq-100) are shown for comparison only. The sector weights apply to the MSCI-based funds (VOX, VGT); the S&P 500 sector SPDRs (XLC, XLK, XLI) hold none of the three until the S&P 500 itself does, and an aerospace-and-defense weight applies only if SpaceX is classified there. Sector classifications were not finalized as of early June 2026 — SpaceX's in particular, and OpenAI's and Anthropic's are as provisional as their listings. Cross-fund views of the private positions are at SpaceX, OpenAI, and Anthropic; fund-level holdings and history are in the fund section.