Same Label, Different Animal: Mandatory Convertibles Inside Preferred Income Funds

Pick two funds that both call themselves "preferred income." One can be ninety percent bank capital securities whose coupons reset with interest rates. Another can hold more than a third of its money in securities scheduled to convert into common stock — Boeing, Oracle, NextEra. Same label, very different things.

The most recent fund filings — the monthly portfolio reports (Form N-PORT) that registered funds submit to the SEC — make the range easy to see. Across the funds that carry "preferred" in their name, the share sitting in mandatory convertibles, preferreds that must turn into equity on a set date, runs from essentially zero to nearly forty percent.

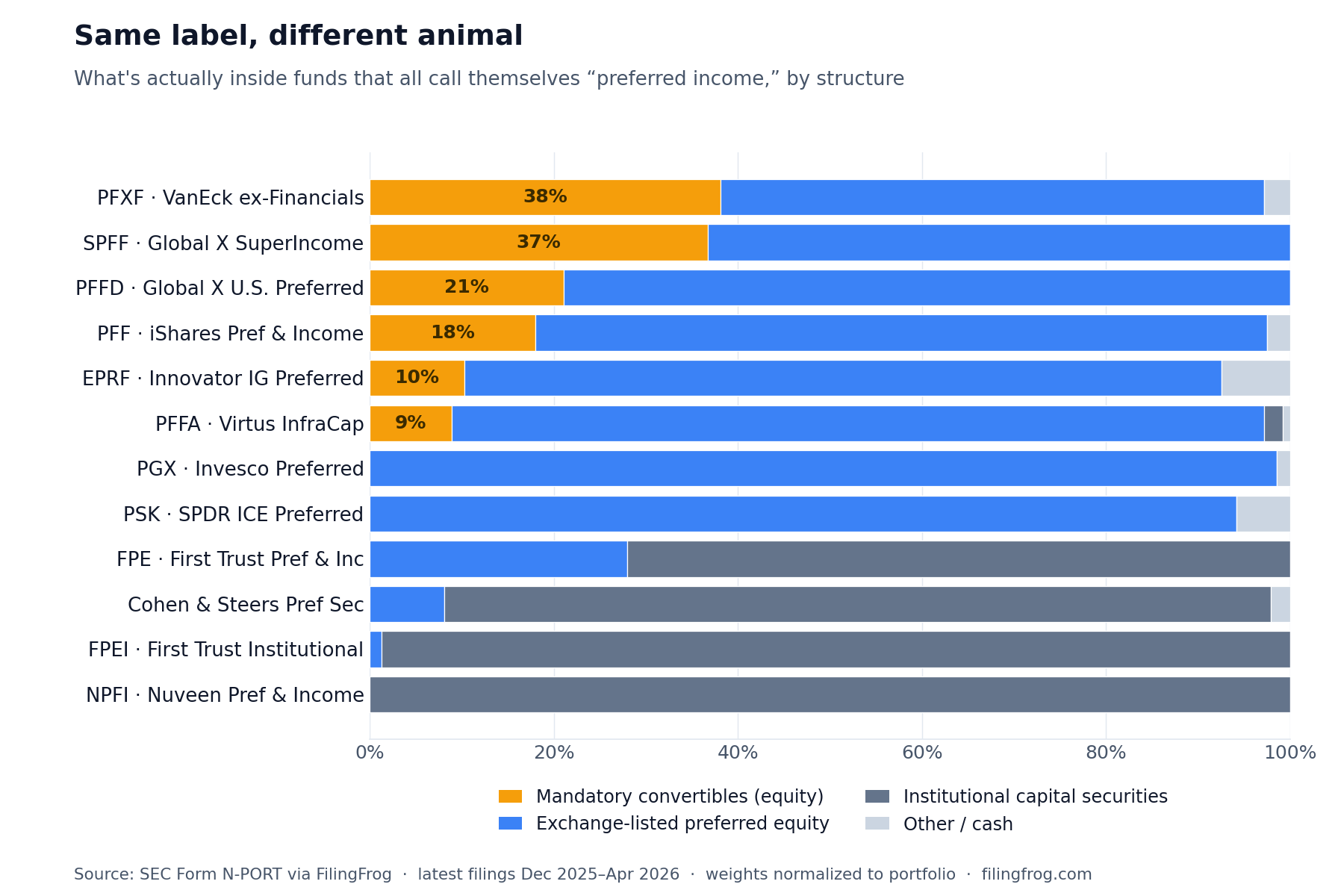

The same label covers very different funds

Ranked by how much of each portfolio is mandatory convertibles, the spread is wide:

- VanEck Preferred Securities ex Financials ETF (PFXF) — 38%

- Global X SuperIncome Preferred ETF (SPFF) — 37%

- Global X U.S. Preferred ETF (PFFD) — 21%

- iShares Preferred and Income Securities ETF (PFF) — 18%

- Innovator S&P Investment Grade Preferred ETF (EPRF) — 10%

- Virtus InfraCap U.S. Preferred Stock ETF (PFFA) — 9%

At the other end, the large active funds hold almost none. The Invesco Preferred ETF (PGX), Cohen & Steers Preferred Securities & Income, and First Trust's institutional fund each sit near zero. Two funds can share the words "preferred income" and own almost nothing in common.

Three different animals under one label

Sorted by structure, "preferred income" splits into three groups that share little beyond the name.

Exchange-listed preferred equity. The retail standard — usually a $25 face value, a fixed dividend, no maturity, callable at par. PGX and PFF are built mostly from these. They carry long duration: in price terms, the position is largely a bet on long-term interest rates.

Institutional capital securities. Junior subordinated debt and bank hybrids, usually $1,000 face value, many with floating or resetting coupons. The active funds live here — Cohen & Steers is about 90% this type, the First Trust Institutional Preferred Securities and Income ETF (FPEI) nearly all of it, and the Nuveen Preferred & Income ETF (NPFI) entirely so. Because many coupons reset, this group carries less rate duration and behaves more like credit.

Mandatory convertibles. Equity on a delay — the group that varies most from fund to fund.

Three funds can each yield around 6% and own three genuinely different things.

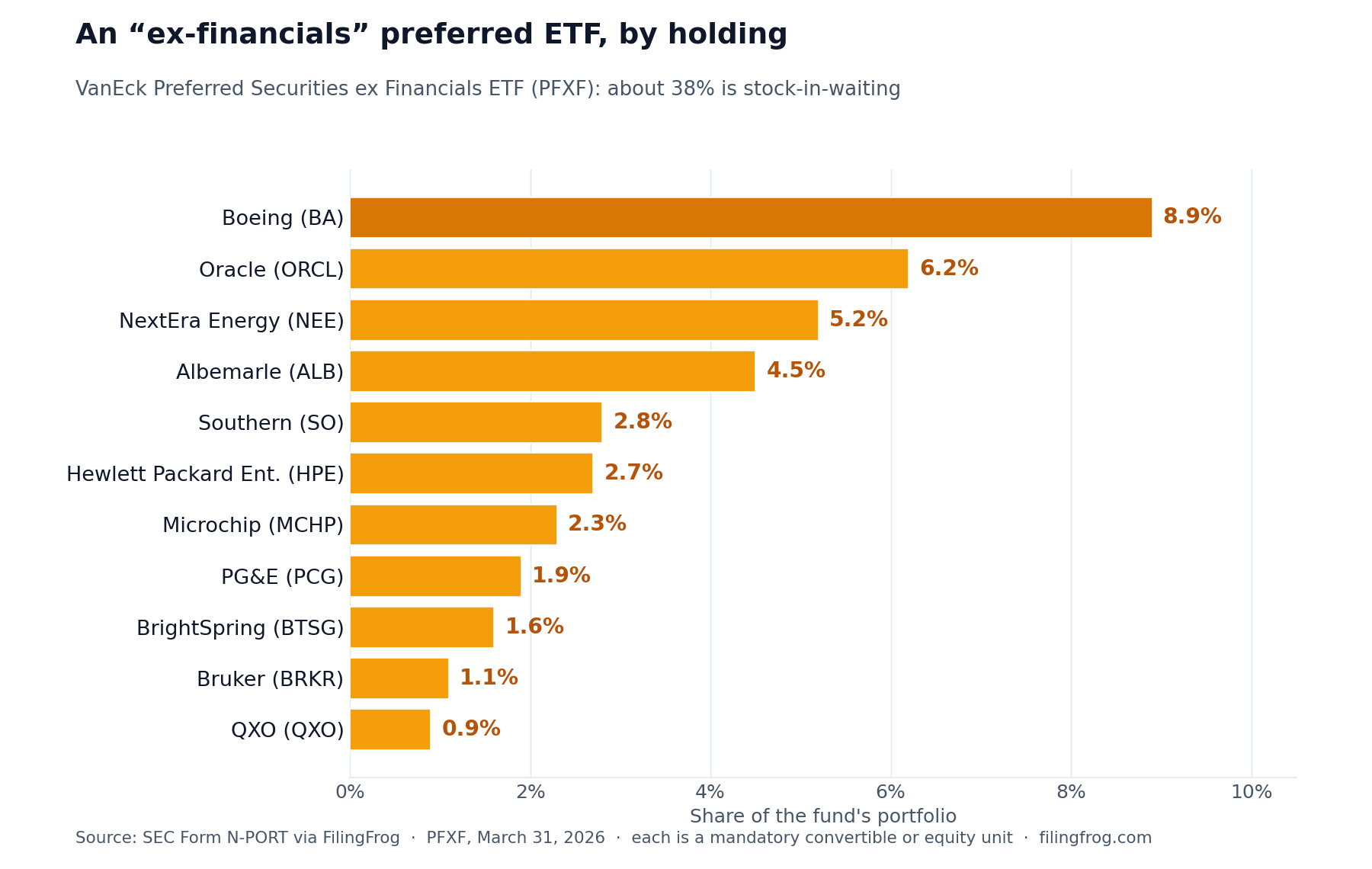

At the far end, a fund that screens out banks

The clearest case is the fund at the top of the list. The VanEck Preferred Securities ex Financials ETF is built to avoid banks — and ends up roughly 38% in securities that will convert into common stock. The reason is almost mechanical: mandatory convertibles are issued mostly by non-financial companies, so screening out the banks and insurers concentrates them rather than avoiding them.

Its largest position is the Boeing (BA) 6% mandatory convertible, near 9% of the fund. Behind it sit Oracle (ORCL), a stack of NextEra Energy (NEE) equity units, Albemarle (ALB), Southern (SO), Hewlett Packard Enterprise (HPE), Microchip Technology (MCHP), and PG&E (PCG).

The convertibles aren't even the whole equity story. The fund's second-largest issuer is Strategy (MSTR), formerly MicroStrategy — about 8% spread across four perpetual preferred series, issued by a company whose principal asset is Bitcoin. Counted alongside the convertibles, close to half of this "preferred" fund moves with equities rather than with rates.

These don't behave like preferreds

A mandatory convertible pays a high fixed dividend for a few years and then, on a scheduled date, converts into common stock — automatically, not at the holder's choice. Boeing's pays 6% and is set to convert around October 15, 2027; until then it earns a coupon, and after that it is the stock. The utility "equity units" from NextEra, Southern, PG&E and PPL (PPL) work the same way: a contract that obliges the holder to buy the company's common shares on a future date.

Three features make them an awkward fit for an income label.

The dividend can be paid in stock. Issuers often hold the right to pay the dividend in common shares rather than cash. A yield on the screen isn't necessarily cash in hand.

The cushion fades with time. Much of the downside protection these offer comes from an embedded options structure that decays as the conversion date nears. Several of these holdings convert within a year or two — Albemarle's in a matter of months — by which point they behave almost entirely like the underlying shares.

Many now trade well above par. After a strong run in the underlying stocks, a number of them trade at large premiums. At those levels there is little downside left to protect, and only partial upside — common equity without full participation.

Why the difference shows up when rates move

Rates are no longer the one-way story they were assumed to be. In June the Federal Reserve held its policy rate at 3.50%–3.75% and, for the first time in a while, its own projections pointed toward possible increases rather than cuts, with the 10-year Treasury near 4.5%. Whichever way rates break from here, the three groups respond differently.

A fund of perpetual preferred equity is, in price terms, a long-duration rate instrument: if long yields rise, the price falls, and a 6% coupon only cushions so much. A fund of resetting institutional capital securities takes less of that hit, because some of its coupons climb as rates climb. And a fund with a large mandatory-convertible sleeve mostly takes its cue from the stock rather than the yield curve — its price rides Boeing, Oracle and NextEra.

That is the part the yield doesn't tell you. The coupon describes the income. The structure describes what the price will do. Two funds wearing the same label, paying nearly the same yield, can move in very different directions — and the only way to tell which is which is to look at what they actually hold.

Explore Fund HoldingsNotes

The universe here is the 51 registered funds with "preferred" in their name and at least $50 million in net assets — about $76 billion combined — drawn from their most recent Form N-PORT filings, which span December 2025 through April 2026 depending on each fund's reporting cycle. Mandatory convertibles were identified by security identifier (CUSIP) and issuer name, then checked against issuer filings, because the disclosures frequently list them only as a company's "preferred stock" or "convertible" — and in some cases with no CUSIP at all. Utility "equity units" and tangible equity units are counted as mandatory because their purchase contracts oblige holders to take common stock on a set date; optional or perpetual convertibles — such as the Wells Fargo and Bank of America series held by some funds, and Strategy's Bitcoin-linked perpetuals — are equity-linked but not mandatory, and are not included in the figures above. Portfolio weights are normalized to each fund's invested assets, and structure is approximated by N-PORT's classification of each holding as preferred equity or debt, which tracks the retail-versus-institutional split closely but is not a literal measure of par value. Fund-by-fund holdings and history are in the fund section, and the underlying companies can be followed through their securities pages.